SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

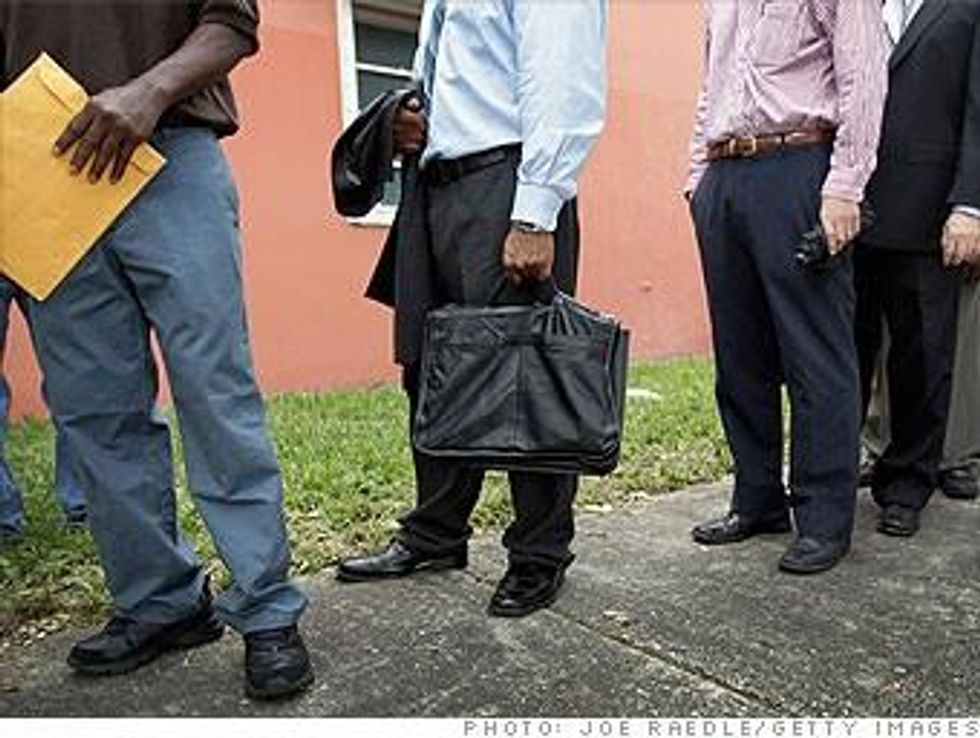

The July jobs report this morning was better than expected, but still bad news. The unemployment rate remains unchanged and the economy is barely treading water. The U.S. would need to create 5 million jobs just to get back to 2007 levels -- yet, of course, millions of young people have since graduated school and entered the workforce (or want to, anyway). So we are talking about a need for way more than 5 million jobs.

Is closing this jobs gap realistic? Or is the United States entering a new phase, similar to what parts of Europe experienced at points in recent decades, in which high unemployment is the norm?

I tend to side with pessimists who say that structural changes in the economy mean that many lost jobs will never come back. But before getting to those arguments, let's consider the optimistic viewpoint that Paul Krugman advances in his book, End This Depression Now.

Here's what Krugman says:

The truth is that recovery would be almost ridiculously easy to achieve: all we need is to reverse the austerity policies of the past couple of years and temporarily boost spending. Never mind all the talk of how we have a long-run problem that can't have a short-run solution--this may sound sophisticated, but it isn't. With a boost in spending, we could be back to more or less full employment faster than anyone imagines.

Krugman suggests that this could be accomplished with familiar policy options like:

increased federal aid to state and local governments, which would restore the jobs of many public employees; a more aggressive approach by the Federal Reserve to quantitative easing (that is, purchasing bonds in an attempt to reduce long-term interest rates); and less timid efforts by the Obama administration to reduce homeowner debt.

Elsewhere, Krugman and others have suggested large-scale investments in infrastructure, which would exploit cheap interest rates and armies of idle construction workers to rebuild roads, bridges, and water systems. (Not to mention bore a new rail tunnel under the Hudson River, a crucial public works project that Gov. Chris Christie gratuitously killed a while back.)

Assuming we could sweep away all the political obstacles, would Krugman's solutions work? The pessimists tend to think not, and among them is Krugman's fellow Nobel laureate, Joseph Stiglitz. In an article in Vanity Fair a few months ago, Stiglitz suggested that today's recession is no ordinary cyclical downturn. Instead, he compared it to the Great Depression, which he suggests was caused in large part by America's shift from an agricultural to an industrial society. Stiglitz argues that the United States has been in a similarly profound transition in recent decades, which accelerated in the Bush years thanks to globalization and other forces:

The fact is the economy in the years before the current crisis was fundamentally weak, with the bubble, and the unsustainable consumption to which it gave rise, acting as life support. Without these, unemployment would have been high. It was absurd to think that fixing the banking system could by itself restore the economy to health. Bringing the economy back to "where it was" does nothing to address the underlying problems.

The unpleasant truth, says Stiglitz, is "that the economy will not bounce back on its own, at least not in a time frame that matters to ordinary people."

One other point to mention, on the pessimistic side of the ledger, is about the nature of the new jobs being created in today's economy. Sure, the U.S. had the "full employment" in 2007, but many of those jobs were lousy, low-wage positions that weren't enabling workers to climb into the middle class. Today, with corporations even better at outsourcing and turning good jobs into bad jobs, new job creation is even more tilted toward positions that pay low wage and include few benefits.

Maybe the debate between the optimists and pessimists doesn't much matter, since the U.S. should take many of the same policy steps regardless. These include not just the short-term stimulus measures Krugman suggests, but other policies that would produce long-term economic growth. What's needed, says Stiglitz, is:

a government stimulus designed not to preserve the old economy but to focus instead on creating a new one. We have to transition out of manufacturing and into services that people want--into productive activities that increase living standards, not those that increase risk and inequality. To that end, there are many high-return investments we can make. Education is a crucial one--a highly educated population is a fundamental driver of economic growth. Support is needed for basic research. Government investment in earlier decades--for instance, to develop the Internet and biotechnology--helped fuel economic growth.

Whether you're an optimist or a pessimist, one thing should be clear: Tomorrow's great era of American prosperity is not going to happen by accident, just like the postwar boom didn't just happen. We need to make it happen with bold public policy.

The July jobs report this morning was better than expected, but still bad news. The unemployment rate remains unchanged and the economy is barely treading water. The U.S. would need to create 5 million jobs just to get back to 2007 levels -- yet, of course, millions of young people have since graduated school and entered the workforce (or want to, anyway). So we are talking about a need for way more than 5 million jobs.

Is closing this jobs gap realistic? Or is the United States entering a new phase, similar to what parts of Europe experienced at points in recent decades, in which high unemployment is the norm?

I tend to side with pessimists who say that structural changes in the economy mean that many lost jobs will never come back. But before getting to those arguments, let's consider the optimistic viewpoint that Paul Krugman advances in his book, End This Depression Now.

Here's what Krugman says:

The truth is that recovery would be almost ridiculously easy to achieve: all we need is to reverse the austerity policies of the past couple of years and temporarily boost spending. Never mind all the talk of how we have a long-run problem that can't have a short-run solution--this may sound sophisticated, but it isn't. With a boost in spending, we could be back to more or less full employment faster than anyone imagines.

Krugman suggests that this could be accomplished with familiar policy options like:

increased federal aid to state and local governments, which would restore the jobs of many public employees; a more aggressive approach by the Federal Reserve to quantitative easing (that is, purchasing bonds in an attempt to reduce long-term interest rates); and less timid efforts by the Obama administration to reduce homeowner debt.

Elsewhere, Krugman and others have suggested large-scale investments in infrastructure, which would exploit cheap interest rates and armies of idle construction workers to rebuild roads, bridges, and water systems. (Not to mention bore a new rail tunnel under the Hudson River, a crucial public works project that Gov. Chris Christie gratuitously killed a while back.)

Assuming we could sweep away all the political obstacles, would Krugman's solutions work? The pessimists tend to think not, and among them is Krugman's fellow Nobel laureate, Joseph Stiglitz. In an article in Vanity Fair a few months ago, Stiglitz suggested that today's recession is no ordinary cyclical downturn. Instead, he compared it to the Great Depression, which he suggests was caused in large part by America's shift from an agricultural to an industrial society. Stiglitz argues that the United States has been in a similarly profound transition in recent decades, which accelerated in the Bush years thanks to globalization and other forces:

The fact is the economy in the years before the current crisis was fundamentally weak, with the bubble, and the unsustainable consumption to which it gave rise, acting as life support. Without these, unemployment would have been high. It was absurd to think that fixing the banking system could by itself restore the economy to health. Bringing the economy back to "where it was" does nothing to address the underlying problems.

The unpleasant truth, says Stiglitz, is "that the economy will not bounce back on its own, at least not in a time frame that matters to ordinary people."

One other point to mention, on the pessimistic side of the ledger, is about the nature of the new jobs being created in today's economy. Sure, the U.S. had the "full employment" in 2007, but many of those jobs were lousy, low-wage positions that weren't enabling workers to climb into the middle class. Today, with corporations even better at outsourcing and turning good jobs into bad jobs, new job creation is even more tilted toward positions that pay low wage and include few benefits.

Maybe the debate between the optimists and pessimists doesn't much matter, since the U.S. should take many of the same policy steps regardless. These include not just the short-term stimulus measures Krugman suggests, but other policies that would produce long-term economic growth. What's needed, says Stiglitz, is:

a government stimulus designed not to preserve the old economy but to focus instead on creating a new one. We have to transition out of manufacturing and into services that people want--into productive activities that increase living standards, not those that increase risk and inequality. To that end, there are many high-return investments we can make. Education is a crucial one--a highly educated population is a fundamental driver of economic growth. Support is needed for basic research. Government investment in earlier decades--for instance, to develop the Internet and biotechnology--helped fuel economic growth.

Whether you're an optimist or a pessimist, one thing should be clear: Tomorrow's great era of American prosperity is not going to happen by accident, just like the postwar boom didn't just happen. We need to make it happen with bold public policy.

The July jobs report this morning was better than expected, but still bad news. The unemployment rate remains unchanged and the economy is barely treading water. The U.S. would need to create 5 million jobs just to get back to 2007 levels -- yet, of course, millions of young people have since graduated school and entered the workforce (or want to, anyway). So we are talking about a need for way more than 5 million jobs.

Is closing this jobs gap realistic? Or is the United States entering a new phase, similar to what parts of Europe experienced at points in recent decades, in which high unemployment is the norm?

I tend to side with pessimists who say that structural changes in the economy mean that many lost jobs will never come back. But before getting to those arguments, let's consider the optimistic viewpoint that Paul Krugman advances in his book, End This Depression Now.

Here's what Krugman says:

The truth is that recovery would be almost ridiculously easy to achieve: all we need is to reverse the austerity policies of the past couple of years and temporarily boost spending. Never mind all the talk of how we have a long-run problem that can't have a short-run solution--this may sound sophisticated, but it isn't. With a boost in spending, we could be back to more or less full employment faster than anyone imagines.

Krugman suggests that this could be accomplished with familiar policy options like:

increased federal aid to state and local governments, which would restore the jobs of many public employees; a more aggressive approach by the Federal Reserve to quantitative easing (that is, purchasing bonds in an attempt to reduce long-term interest rates); and less timid efforts by the Obama administration to reduce homeowner debt.

Elsewhere, Krugman and others have suggested large-scale investments in infrastructure, which would exploit cheap interest rates and armies of idle construction workers to rebuild roads, bridges, and water systems. (Not to mention bore a new rail tunnel under the Hudson River, a crucial public works project that Gov. Chris Christie gratuitously killed a while back.)

Assuming we could sweep away all the political obstacles, would Krugman's solutions work? The pessimists tend to think not, and among them is Krugman's fellow Nobel laureate, Joseph Stiglitz. In an article in Vanity Fair a few months ago, Stiglitz suggested that today's recession is no ordinary cyclical downturn. Instead, he compared it to the Great Depression, which he suggests was caused in large part by America's shift from an agricultural to an industrial society. Stiglitz argues that the United States has been in a similarly profound transition in recent decades, which accelerated in the Bush years thanks to globalization and other forces:

The fact is the economy in the years before the current crisis was fundamentally weak, with the bubble, and the unsustainable consumption to which it gave rise, acting as life support. Without these, unemployment would have been high. It was absurd to think that fixing the banking system could by itself restore the economy to health. Bringing the economy back to "where it was" does nothing to address the underlying problems.

The unpleasant truth, says Stiglitz, is "that the economy will not bounce back on its own, at least not in a time frame that matters to ordinary people."

One other point to mention, on the pessimistic side of the ledger, is about the nature of the new jobs being created in today's economy. Sure, the U.S. had the "full employment" in 2007, but many of those jobs were lousy, low-wage positions that weren't enabling workers to climb into the middle class. Today, with corporations even better at outsourcing and turning good jobs into bad jobs, new job creation is even more tilted toward positions that pay low wage and include few benefits.

Maybe the debate between the optimists and pessimists doesn't much matter, since the U.S. should take many of the same policy steps regardless. These include not just the short-term stimulus measures Krugman suggests, but other policies that would produce long-term economic growth. What's needed, says Stiglitz, is:

a government stimulus designed not to preserve the old economy but to focus instead on creating a new one. We have to transition out of manufacturing and into services that people want--into productive activities that increase living standards, not those that increase risk and inequality. To that end, there are many high-return investments we can make. Education is a crucial one--a highly educated population is a fundamental driver of economic growth. Support is needed for basic research. Government investment in earlier decades--for instance, to develop the Internet and biotechnology--helped fuel economic growth.

Whether you're an optimist or a pessimist, one thing should be clear: Tomorrow's great era of American prosperity is not going to happen by accident, just like the postwar boom didn't just happen. We need to make it happen with bold public policy.