SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

Nearly a decade before she was the public face of DHS, Noem’s tall tales about the estate tax helped gut one of the few remaining checks on elite fortunes.

Kristi Noem will no longer be the face of the Department of Homeland Security, labeling peaceful citizens defending liberty as “domestic terrorists.” President Donald Trump is now appointing her to a new position of “special envoy in the Western Hemisphere.”

Wherever she goes next, we should remember her DHS debacle wasn’t her first deception rodeo. It turns out that Noem has a long history of twisting the truth to serve the powerful.

In 2017, nearly a decade ago, we caught then-Rep. Kristi Noem (R-SD) telling a whopper fib about her family’s experience with the estate tax—or what Noem called the “death tax.”

The estate tax, our nation’s only levy on the inherited wealth of multimillionaires and billionaires, has been in place since 1916. In its first half century, it helped put a brake on the build-up of concentrated wealth and power, discouraging dynastic fortunes that threatened democracy.

It’s strangely fitting that Noem, who now slanders law-abiding immigrants and the citizens defending them as “domestic terrorists,” played a big role in gutting those taxes on the rich.

But for the last 30 years, the estate tax has been under right-wing assault, including a steady drumbeat for its repeal. And one tactic they’ve used is to claim the tax applies to small farmers and other working Americans, rather than the tiny percentage of extremely wealthy estates it actually targets—exclusively multimillionaires and billionaires, the top 0.01%

Noem’s personal political narrative, repeated at town hall meetings during her 2010 campaign for Congress, is a yarn about a rapacious and greedy federal government imposing an estate tax on her struggling family.

In a 2015 speech on the House Floor and in a 2016 op-ed for Fox News, Noem repeated the estate tax story. After her father died, Noem claimed, “We got a bill in the mail from the IRS that said we owed them money because we had a tragedy that happened to our family.”

“We could either sell land that had been in our family for generations or we could take out a loan,” Noem said, adding that “it took us 10 years to pay off that loan to pay the federal government those death taxes.” Noem says the episode was “one of the main reasons I got involved in government and politics.”

In December 2017, Noem was appointed by then-House Majority Leader Paul Ryan (R-Wis.) to the joint committee working to reconcile the 2017 Trump tax bill—which at the time included a proposal to eliminate the federal estate tax altogether.

That month, I published a widely circulated op-ed about Noem in USA Today arguing that “her sad family saga doesn’t add up.”

My commentary surfaced several simple facts: The federal estate tax has a 100% exemption for spouses. In other words, if a spouse dies, the estate’s assets go to the surviving spouse without any estate tax. Corinne Arnold, Kristi Noem’s mother, was alive during these years. (In fact, she is still alive now at 78 years and was active in Kristi’s second campaign for South Dakota governor in 2022.)

Estate tax attorney Bob Lord noted at the time: “It’s hard to believe the estate of a farmer who died in 1994 and was survived by his spouse was subject to the tax. It easily could have been deferred. That would have been a no-brainer.”

Moreover, the process of filing a return can be extended for years, especially for operating farms.

The combination of family tragedy and populist outrage makes for a potent partisan story, but veers from the truth. In the years she campaigned as a victim of the estate tax, Noem’s family actually cashed millions in government farm subsidies. Between 1995 and 2024, her family’s Racota Valley Ranch in Hazel, South Dakota deposited $4.9 million in government subsidy checks.

A few days after my USA Today article, the Argus Leader, South Dakota’s biggest statewide newspaper, wrote an editorial: “Time for Kristi Noem to Get Her Tax Story Straight.” In her now well-known deflective fashion, Noem fired back that it was “fake news.”

If Noem’s estate tax story is true, she could easily put our doubts to rest. She could explain why her family didn’t use a spousal exemption, share a redacted “bill” from the IRS, or disclose who provided the loan she allegedly received. But she hasn’t.

In the meantime, Noem has helped gut the estate tax, contributing to the growing concentration of wealth that threatens our economy and democracy.

Under the Trump tax bill Noem worked on, the federal estate tax now exempts the first $15 million of wealth for an individual and $30 million for a couple. And as governor of South Dakota, Noem fortified the state’s role as a trust haven, attracting billionaires interested in forming dynasty trusts to hide wealth and use loopholes to avoid federal taxes.

The Trump administration and its allies have blamed immigrants for all manner of social ills—including struggling schools, expensive housing and healthcare, and more. In reality, the blame more often lies with extremely wealthy people who won’t pay their fair share of taxes to support public programs.

So it’s strangely fitting that Noem, who now slanders law-abiding immigrants and the citizens defending them as “domestic terrorists,” played a big role in gutting those taxes on the rich.

These lies—about the estate tax, about immigrants, about protesters—have something in common: They protect the powerful. As lawmakers attempt to hold Noem accountable for the reckless activities of Immigration and Customs Enforcement—and consider her for future jobs—they should keep this early story in mind.

"Americans will pay a steep price if Republicans move forward with this disastrous agenda," said Sen. Ron Wyden.

The House Republican Study Committee on Tuesday released a blueprint for a new budget reconciliation package with the purported goal of making "life more affordable for working families."

However, according to an analysis by Washington Post economic policy reporter Jacob Bogage, two of the three most expensive items in the GOP budget blueprint would be the elimination of the federal estate tax, which would provide a massive windfall to the richest US households, and indexing capital gains to inflation, which even the conservative American Enterprise Institute contends "would further distort taxpayer decisions and increase the ability to shelter income from taxation."

Other items in the GOP blueprint include refilling the Strategic Petroleum Reserve with oil seized from Venezuela, blocking federal funds for abortion providers, and a new "excise tax on colleges that allow trans women in sports."

Sen. Ron Wyden (D-Ore.), ranking member of the Senate Finance Committee, wasted no time ripping the proposal from the largest right-wing House caucus to pieces.

"After passing the largest health care cut in American history, Republicans are doubling down on a failed agenda that benefits billionaires and giant corporations while ripping away food, healthcare and other basic necessities,” Wyden said. “This legislation will eliminate protections for Americans with preexisting conditions, place more red tape between families and their healthcare, and seize ideological trophies instead of focusing on making life more affordable. Americans will pay a steep price if Republicans move forward with this disastrous agenda.”

Richard Phillips, pensions and tax policy director for Sen. Bernie Sanders (I-Vt.), marveled at the GOP loading up a bill supposedly focused on working families with massive giveaways to the wealthiest Americans.

"As part of it's new affordability agenda for the American people the Republican Study Committee reveals its plan to give the wealthiest 0.2% of estates a $281 billion tax break?" he wrote in a post on X.

Chuck Marr, vice president of federal tax policy at the Center on Budget and Policy Priorities, similarly called the GOP blueprint "tone deaf."

"Nothing says attack the affordability crisis working-class people face than Rs calling for eliminating the estate tax for the wealthiest heirs in the country—just months after giving them a $30 million tax free exemption," he wrote.

The GOP's second attempt at a budget reconciliation package comes months after it passed the One Big Beautiful Bill Act, a reconciliation package that gave more tax breaks to the rich, but cut Medicaid spending by nearly $1 trillion over the next decade, while also slashing spending on the Supplemental Nutrition Assistance Program by nearly $200 billion over the same period.

The Republican's policy will continue a decades-long effort to weaken a critical tool to prevent the hoarding of wealth from one generation to the next.

The sprawling tax and spending bill before the House of Representatives would cut more than $200 billion from food assistance, potentially affecting 4 million children and 7 million adults, while providing an estate tax cut costing roughly the same amount to a few thousand people who will leave behind more than $7 million to their heirs.

The bill would increase the estate tax exemption to $15 million for single people and $30 million for couples in 2026 and allow it to rise with inflation moving forward. In other words, a couple could leave $29.99 million to their heirs in 2026 without paying a cent of estate tax.

This would continue a decades-long effort to weaken a critical tool to prevent the hoarding of wealth from one generation to the next.

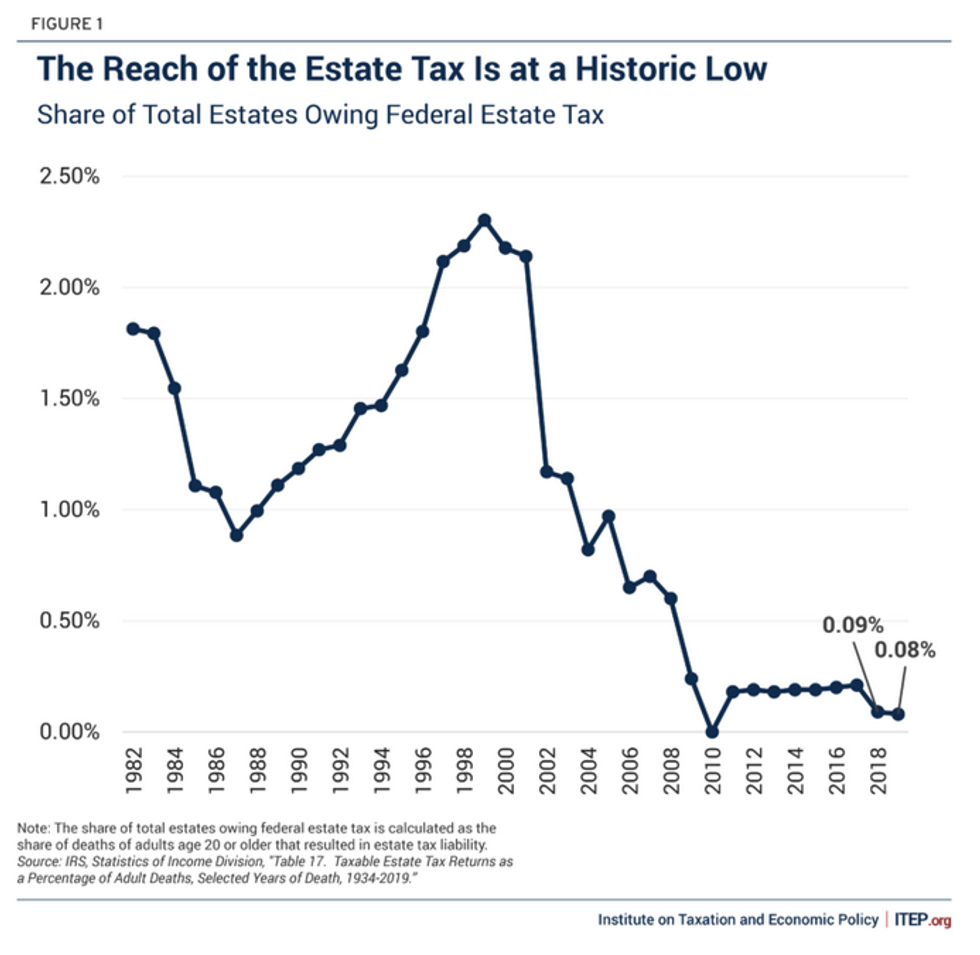

Less than a generation ago, the estate tax was much more robust, with an individual exemption of $675,000 in 2001. Adjusted for inflation, that would amount to an exemption of $1.2 million per individual today. Even so, the tax was paid by just a tiny fraction of Americans; just 2.14 percent of all estates were subject to the tax in 2001.

But since then, lawmakers have weakened the estate tax four times, most significantly via the 2017 Trump tax law. That law doubled the estate tax exemption, bringing it to about $14 million today ($28 million for couples). This would revert to roughly $7 million if the Trump tax provisions expire at the end of this year as scheduled.

As we explained in a 2023 report, these cuts have taken the tax to historic lows. The most recent data from the IRS, from 2019, show that just 0.08 percent of all deaths resulted in estate tax liability that year, when the estate tax had an exemption of $11.4 million per person.

People across the country, including many Republicans, are expressing concern about the breadth and depth of proposed cuts to food assistance, health care, and other public services that are part of the reconciliation package the House is currently moving forward. At the same time, overwhelming majorities of Americans think that wealth inequality is a problem that leaders need to solve.

Given this, the least that lawmakers can do is allow the estate tax to drop slightly back down in 2026 instead of cutting it for the wealthiest families yet again.

"The unavoidable truth is that Republicans' core priority with this legislation was to benefit the wealthy at the expense of everyone else, and that is exactly what their bill does," said Democratic Rep. Don Beyer.

House Republicans on Wednesday advanced legislation that would deliver a slew of tax breaks to the wealthiest Americans and large corporations, giveaways that the party aims to fund with unprecedented cuts to Medicaid and federal nutrition assistance.

Throughout the marathon markup hearing that began Tuesday afternoon and ended with Wednesday morning's party-line vote, Democratic members of the House Ways and Means Committee offered amendments aimed at closing the carried-interest loophole, preventing a major tax break for rich heirs, blocking any handouts to centimillionaires, and reverting the top marginal tax rate to its pre-2017 level of 39.6%.

Republicans—many of whom stand to reap significant personal benefits from another round of tax cuts—rejected the Democratic amendments.

"At every turn, Republicans voted down amendments designed to prevent the majority of benefits of their tax bill from flowing to rich people," Rep. Don Beyer (D-Va.), a member of the committee, said following Wednesday's vote. "The unavoidable truth is that Republicans' core priority with this legislation was to benefit the wealthy at the expense of everyone else, and that is exactly what their bill does."

Shortly after the hearing kicked off on Tuesday, the nonpartisan Joint Committee on Taxation released a distributional analysis showing that the Republican tax bill—part of the GOP's sprawling reconciliation package—would disproportionately benefit the wealthiest Americans while doing little for low- to middle-income families.

Beyer noted on social media that "a dirty little secret" of the Republican tax legislation is that it would actually raise taxes on the bottom 20% of Americans in 2029—the year President Donald Trump leaves office.

The bill is even more regressive when you look at 2029 when tax cuts for families expire & tax increases resulting from cuts to ACA premium tax credits grow larger. pic.twitter.com/3BDz1bFina

— Brendan Duke (@Brendan_Duke) May 14, 2025

The House Ways and Means Committee vote came as Republicans on the Energy and Commerce and Agriculture Committees simultaneously worked to advance their respective sections of the GOP reconciliation package, the centerpiece of Trump's legislative agenda.

The bills before the latter two committees would enact combined cuts of around a trillion dollars to Medicaid and the Supplemental Nutrition Assistance Program over the next decade, stripping critical benefits from millions of people across the country.

Kobie Christian, a spokesperson for the Unrig Our Economy coalition, said Wednesday that the GOP reconciliation package is "a reverse Robin Hood of the highest order."

"From cutting healthcare to ripping away food assistance to rubberstamping cost-raising tariffs, Republicans in Washington are making life more expensive for working- and middle-class Americans by handing over their tax dollars to the super-rich," said Christian. "Families need lower costs, not cuts to healthcare and billionaire tax breaks. Congress should be fighting to help working families, not the ultra-wealthy."

Please ignore the tales of horror that apologists for the ultra-rich concoct to advocate against any meaningful tax increases on their deep-pocketed friends.

What is the mission of the Washington, D.C.-based Tax Foundation? Even a quick review of the Tax Foundation’s output makes it perfectly plain: to help make average Americans see the richest among us as terribly overtaxed.

Hardly a Tax Foundation report goes by without one iteration or another of this overtaxed claim. Just last fall, the Tax Foundation produced a study that had billionaire Warren Buffett paying taxes at a rate of over 1,000 percent.

A few years back, early in the Biden years, I deconstructed another Tax Foundation claim, that the passage of tax changes the Biden White House was then pushing would leave the estate of a hypothetical taxpayer worth $100 million facing a tax rate of 61.1 percent. My response detailed the absurdity of that claim.

But what if that 61.1 percent had turned out to be an appropriate calculation? Would that 61.1 percent rate have really amounted to an oppressive tax levy? The Tax Foundation sure wants people to think so.

So let’s take a closer look at the Tax Foundation’s mythical ultra-rich taxpayer and let’s tweak the Tax Foundation’s hypothetical facts to make them just realistic enough to work with.

Suppose we assume our mythical taxpayer originally paid $1 million for the asset that ended up worth $100 million at her death 25 years later. That would leave $99 million of taxable gain. And a $1 million asset appreciating to $100 million after 25 years would have an average annual rate of return of 20.23 percent, a realistic rate for the sort of “home run investments” the ultra-rich actually make.

Let’s also ignore the exemption from federal estate tax — currently $14 million per individual, $28 million for a married couple — and treat the entire amount remaining from the $100 million after payment of income tax as subject to a 40 percent estate tax.

Applying the Tax Foundation’s methodology from that point, we would end up with a total effective tax rate just shy of 65.8 percent, nearly five percentage points higher than the 61.1 percent rate that had our friends at the Tax Foundation clutching their pearls. Wow! Sounds stunningly oppressive, huh?

Actually, no. The reason: The Tax Foundation’s presentation deceptively ignores the tax reduction magic of buy-hold for decades-sell, the tax loophole that causes the effective annual tax rate on the growth in the value of investments to decline as the rate of return and length of the holding period increase.

Our mythical taxpayer would be the quintessential beneficiary of this tax reduction magic. She would see her investment gains compound for 25 years without paying a nickel in income tax, all while her asset’s value was increasing by 20.23 percent per year.

The Tax Foundation, you see, makes quite the fuss over the one-time tax a mythical taxpayer’s estate would pay in the year of her death, but conveniently forgets about the taxpayer’s zero tax rate for the previous 25 years running.

That focus on a once-in-25-years tax payment ignores the full picture. To see that more clearly, consider the impact that a 65.8 percent tax would have on a mythical taxpayer’s overall investment return. At an after-tax annual rate of return of 15.18 percent, an asset with an initial value of $1 million will be worth $34.2 million in 25 years, exactly the amount left of the mythical taxpayer’s $100 million after her estate’s one-time tax payment of $65.8 million. That would be a 25 percent reduction in the pre-tax annual rate of return of 20.23 percent.

In other words, that supposedly onerous 65.8 percent tax at the time of the Tax Foundation’s mythical taxpayer’s death translates to an effective annual tax rate of just 25 percent.

Had the Tax Foundation’s mythical taxpayer been required to pay federal tax, covering both current income tax and future estate tax, at an annual rate of 25 percent on the growth in her investment’s value, and had she sold off just enough of the investment each year to pay the tax, her estate would be left with the same amount in the year of her death as it would have after paying the supposedly oppressive income and estate tax due under the terms of the Biden budget.

So, to review, the Tax Foundation concocted a hypothetical situation to show the proposals in Biden’s budget rated as extreme and oppressive. But even though that hypothetical is so concocted it couldn’t be found in the real-life situations of even the richest Americans, the supposedly oppressive one-time tax rate paid by the Tax Foundation’s mythical taxpayer translates to a modest effective annual tax rate of just 25 percent.

The bottom line: Once we take into account the impact of buy-hold for decades-sell, the tales of horror that apologists for the ultra-rich concoct to advocate against any meaningful tax increases on their deep-pocketed friends turn out to be not at all horrible.

Unless you’re horrified at the prospect of a reformed tax system that prevents the already obscene concentration of American wealth from becoming even worse.

While purporting to be concerned about income inequality, Johnson advocates for proposals obviously intended to benefit his rich benefactors and, worse yet, himself.

If you were a rich Wisconsinite striving to get even richer and you had little regard for intellectual honesty or the well-being of your fellow citizens, you would agree with Sen. Ron Johnson’s remarks at last month’s Senate Finance Committee hearing.

Otherwise, you’d find the senator’s views troublesome, to say the least.

I was a witness at that hearing. Johnson asked me to agree with him that having both an income tax and an estate tax is double taxation. As politely as I could, I pointed out that the income tax and the estate tax are two different taxes. The senator’s argument is no different than saying it is double taxation if an average American, after paying tax on her wages, pays federal excise tax at the pump when she purchases gas.

Unless and until Johnson’s face replaces Roosevelt’s at Mt. Rushmore, I’ll go out on a limb and say we should stick with the tax structure Roosevelt advocated.

Johnson undoubtedly knows better. America has had both an estate tax and an income tax for over a century now. They’re two different taxes. One is an income tax; the other is an excise tax on the transfer of substantial wealth. The specific purpose of the estate tax was to limit the size of America’s largest dynastic fortunes, lest we slip into an aristocracy. The lead advocate for the estate tax, President Teddy Roosevelt, recognized the necessity for both taxes: “The really swollen fortune, by the mere fact of its size,” Roosevelt observed, “acquires qualities which differentiate it in kind as well as in degree from what is possessed by men of relatively small means.” Therefore, Roosevelt, a Republican like Johnson, advocated for both a “graduated income tax on big fortunes,” and “a graduated inheritance tax on big fortunes, properly safeguarded against evasion, and increasing rapidly in amount with the size of the estate.”

At the hearing, Johnson was speaking in support of keeping one of the worst loopholes in the tax code, a provision commonly known as stepped-up basis. It allows the untaxed gains on the investment assets of mega-millionaires and billionaires to escape income taxation entirely, as long as they hold those assets until death. Jeff Bezos, for example, would avoid income tax on over $100 billion of gain on his Amazon shares were he to hold those shares until his death. And if ultra-rich Americans ever need cash, they don’t need to sell highly appreciated assets. Instead, they can borrow against the assets. It’s a strategy known as buy-borrow-die.

Johnson’s true goal isn’t really protecting the ultra-rich from double taxation, though. He actually wants to protect them from any taxation. That’s what the Death Tax Repeal Act of 2023, a bill Johnson and 41 other Republican senators have sponsored, would do. If that were to become law, Mr. Bezos, or any other billionaire, could pass his billions to his inheritors free of both estate tax and income tax on all those previously untaxed gains.

Unless and until Johnson’s face replaces Roosevelt’s at Mt. Rushmore, I’ll go out on a limb and say we should stick with the tax structure Roosevelt advocated. And that requires closing the stepped-up basis loophole.

At the hearing, Johnson did not limit his shilling for the ultra-rich to the stepped-up basis issue. While purporting to be concerned about income inequality, Johnson advocated for proposals obviously intended to benefit his rich benefactors and, worse yet, himself. Were it up to him, for example, our tax law would “index out” inflationary gains. Here’s how that would work for Johnson and his fellow real estate moguls: Say Johnson purchased a property for $10 million with $2 million in cash and an $8 million loan, using the property’s rental income to make the loan payments. Now, say inflation ran at 4% for 10 years and Johnson’s property kept pace. Under his plan, he’d be treated as if he paid $14 million for the property. And if he then sold the property for its $14 million value? He’d have no income tax to pay, but after paying off the loan, he’d have a $4 million profit. Yes, $800,000 of that profit would be attributable to inflation, but the other $3.2 million would be real profit, and it would escape tax entirely if Johnson has his way.

Johnson’s efforts to “address inequality”—yes, he really presented it this way at the hearing—aren’t limited to opposing stepped-up basis reform and advocating for indexing for inflation. He also insists that he and his rich patrons not be taxed on their massive investment gains until they sell assets so they have the “wherewithal to pay.” That would allow the country’s ultra-rich to continue to benefit from the tax-free compounding of their investment gains using the buy-borrow-die strategy. When you do the math, even when the ultra-rich sell long-held investments before they die and pay tax on their gains, the effective annual rate of tax on the growth in their wealth can be less than 5%. With Johnson’s plan to “index out” inflation added to his staunch support of buy-borrow die, that effective rate would be even lower.

There’s no need to guess about whether Johnson believes he’s advocating for good tax policy or is simply carrying water for his billionaire backers (and himself). The record is clear. In 2017, Johnson pushed hard for the so-called “pass-through deduction,” which allows owners of limited liability companies and subchapter S corporations to pay a 20% lower rate of tax on their income. He even threatened to withhold his vote for former President Donald Trump’s tax package unless the pass-through deduction was increased. In 2018, according to reporting by ProPublica, the pass-through deduction generated tax deductions of over $117 million for Dick and Liz Uihlein, the owners of Uline, and over $97 million for Diane Hendricks, the owner of ABC Supply Co. In 2022, according to the Milwaukee Journal Sentinel, Hendricks and the Uihleins contributed at least $22.5 million to Wisconsin Truth PAC, a Johnson-supporting super PAC which spent $24 million on ads attacking Johnson’s 2022 opponent, Mandela Barnes.

Those massive contributions were entirely rational, in a depressing way that reeks of corruption. In 2018 alone, Hendricks and the Uihleins saved just under $80 million in tax as a result of Johnson’s handiwork. His efforts to continue the pass-through deduction past its scheduled 2025 expiration date could net them about $1 billion over the next decade. That $22.5 million they spent on Johson’s 2022 senate campaign may be categorized as a campaign contribution. But when $22.5 million has the potential to enrich you to the tune of $1 billion, it smells a lot more like an investment. And a highly profitable one; the kind only billionaires experience.

With Washington filled with politicians like Ron Johnson, we need more patriotic millionaires. A lot more. To paraphrase our Vice Chair, Stephen Prince, we need more wealthy Americans to step up and say that while they like being rich, they recognize that our tax system has been rigged in their favor for far too long. And we need more politicians fighting to unrig our tax system, not rig it further. We’ll never change the mindset of Ron Johnson and his ilk. The only way to fix this mess is to elect politicians who will outvote them.

Trump-Vance tax agenda of cuts and tariffs stands in stark contrast to the reforms that Walz has shepherded.

As Minnesota Gov. Tim Walz and Ohio Sen. JD Vance prepare to debate this week, it’s worth looking at their approaches to tax policy, a critical throughline that helps determine not only the quality of public services in communities across the country, but also the overall fairness of our economy.

Recent reforms signed by Walz have helped create a moderately progressive tax system in Minnesota, making the state stand apart from most that charge the rich lower tax rates than everyone else.

Our analysis shows that taxes on working-class families declined markedly over the last few years in Minnesota while taxes on high-income people went up slightly.

The most notable changes were signed into law by Walz in 2023 as part of a sweeping tax reform package. Some changes were temporary, like taxpayer rebate checks and expanded property tax credits. But the bill also included important permanent reforms.

In Minnesota, Walz has helped institute a tax system that asks wealthy households and profitable corporations to chip in more to help create a stronger, healthier, more equitable society.

Chief among those was a new Child Tax Credit that is expected to slash child poverty in Minnesota by one-third, according to Columbia University’s Center on Poverty and Social Policy. The link between Child Tax Credits and child well-being is well established, as the financial security afforded by these credits is associated with improved child and maternal health, better educational achievement, and stronger future economic outcomes.

Other tax cuts signed by Walz include expanded exemptions for Social Security income and for student loan forgiveness, plus an extension of the Child Care Tax Credit to newborn children.

To help pay for all this, the 2023 bill included tax increases on high-income people and profitable corporations. Certain tax deductions claimed by high-income filers have been scaled back. Capital gains, dividends, and other investment income over $1 million per year is now subject to a modest 1% surtax. And multinational corporations reporting income overseas now face higher taxes as well, as the state opted to piggyback on a law written by congressional Republicans targeting companies’ “low-taxed income.”

Vance has not been a lawmaker for long and doesn’t have a robust track record on tax policy. The roughly dozen tax-related bills he sponsored or co-sponsored in Congress run the gamut. He has introduced bills that would use the tax code to fight the culture war against colleges, universities, and campus protesters. He’s signed onto several bills that would further enrich the richest, like eliminating the estate tax (which is paid almost exclusively by those inheriting more than $20 million) and making the 2017 Trump tax law’s subsidy for pass-through businesses permanent (which goes mostly to millionaires, who often game the system to extract the largest possible windfalls from this law).

Vance has also introduced legislation to repeal tax incentives for electric vehicles and replace them with tax breaks for buying American-manufactured vehicles, and signed onto a bill to eliminate rebates for upgrading to more efficient appliances. He’s also a co-sponsor of a bill to erode K-12 public schools with private school voucher tax credits.

In August, Vance floated increasing the Child Tax Credit to $5,000 per child for “all American families,” yet details remain scarce. His comments suggest he would make the credit available for many–but not all–the low-income families who currently earn too little to receive it as well as the wealthy families who earn too much (over $400,000). It’s unclear if Vance’s plan would help all low-income families currently left out by the credit’s lack of refundability–he’s never addressed that. While it’s promising that Vance talked about the Child Tax Credit, it’s hard to take his vague proposal seriously–especially after he sat out a vote in the Senate for a bipartisan bill that would have expanded this credit.

On the trail, Vance is hyping up many of his running mate’s tax proposals, including Trump’s tariff tax. This proposal–which would create a 60% tariff on Chinese imports and a 20% one on all other imports–would cost an average middle-class American family nearly $4,000 a year.

The tariff plan is a critical part of the Trump-Vance tax agenda because it’s one of a very small number of revenue raisers in a basket of special interest tax cuts. So, yes, it would help pay for some of those tax cuts (though at an estimated $2.8 trillion raised over the next decade it pales in comparison to the over $9 trillion in revenue loss from proposed cuts). But it would do it in a way that falls hardest on regular families, making our system fundamentally less fair in the process.

That stands in stark contrast to the reforms that Walz has shepherded. In Minnesota, Walz has helped institute a tax system that asks wealthy households and profitable corporations to chip in more to help create a stronger, healthier, more equitable society.

This is the type of tax system that most Americans say they want. It’s also exactly the kind that America desperately needs.

"Over and over again, Republicans in Washington have professed their deep concern about the national debt and yet virtually all of them have signed onto legislation that would provide a $1.8 trillion tax giveaway to billionaires."

Sen. Bernie Sanders on Tuesday unveiled legislation that would hike taxes on estates worth more than $3.5 million as congressional Republicans work to repeal the estate levy entirely—a move that would hand nearly $2 trillion to the wealthiest people in the United States.

The For the 99.5 Percent Act, which Sanders (I-Vt.) unveiled alongside Sen. Elizabeth Warren (D-Mass.) and Rep. Jimmy Gomez (D-Calif.), would impose a 45% tax on estates worth between $3.5 million and $10 million, a 50% tax on estates worth between $10 million and $50 million, a 55% tax on estates worth between $50 million and $1 billion, and a 65% tax on estates valued at over $1 billion.

"This is not a radical idea," Sanders' office said in a press release. "In fact, from 1941-1976, the top estate tax rate was 77% on estates worth more than $50 million."

The new legislation would not impose any new taxes on 99.5% of Americans.

"Over and over again, Republicans in Washington have professed their deep concern about the national debt and yet virtually all of them have signed onto legislation that would provide a $1.8 trillion tax giveaway to billionaires by repealing the estate tax," Sanders said in a statement Tuesday, referring to the GOP's Death Tax Repeal Act of 2023, a bill led by Sen. John Thune (R-S.D.).

Thune's legislation currently has 40 Republican cosponsors, including Senate Minority Leader Mitch McConnell (R-Ky.), whose wife received an inheritance worth between $5 million and $25 million following her mother's death in 2007.

Dozens of House Republicans have also backed legislation that would repeal all federal income taxes and replace them with a regressive national sales tax.

"At a time of massive wealth and income inequality, we need to make sure that people who inherit over $3.5 million pay their fair share of taxes," said Sanders. "We do not need to provide a huge handout to multi-millionaires and billionaires. It is unacceptable that working families across the country today are struggling to file their taxes on time and put food on the table, while the wealthiest among us profit off of enormous tax loopholes and giant tax breaks."

According to a summary released by Sanders' office, the new legislation would also target loopholes and inadequate rules that have allowed billionaire families like the Waltons to pass down wealth tax-free.

The bill was introduced with the backing of more than 420 national, state, and local groups, including the AFL-CIO and Public Citizen.

"For years, billionaires and multi-millionaires have gotten away with paying little to nothing in taxes," Warren said Tuesday. "This legislation will help us fix our broken tax system by closing loopholes that the ultra-wealthy use to dodge paying their fair share. Congress should pass this bill so we can invest in working families and build a brighter future for all of our children."

Citing an estimate from the Joint Committee on Taxation, Sanders' office noted that a previous version of the For the 99.5 Percent Act would have raised $430 billion in federal revenue over its first decade.

The new bill, which faces long odds in both chambers of Congress, was unveiled on Tax Day, an occasion that—as one group put it in a statement earlier Tuesday—serves as "an annual reminder that the ultra-rich exist in an entirely separate world when it comes to taxes."

The For the 99.5 Percent Act is one of several pieces of legislation mentioned by the Patriotic Millionaires in its newly released tax reform agenda, which calls for wealth taxes, a 90% top tax rate on centimillionaires, and other changes to "fundamentally reimagine our tax code."

"For our future, our grandchildren's future, and our country's future," the group said Tuesday, "we must tax the rich."

Survey data released Tuesday by the progressive advocacy group Groundwork Action found that nearly 75% of U.S. voters, regardless of party affiliation, want Congress to prioritize cracking down on wealthy tax cheats and closing loopholes that benefit the rich.

The polling data also showed that 70% of U.S. voters want Congress to "make sure millionaires and billionaires pay more in taxes."

"Voters across the political spectrum are tired of hearing about billionaires and massive corporations paying less in taxes than nurses, teachers, or firefighters, so it's no surprise they're rejecting the Republican agenda of protecting tax breaks for the wealthy at all costs," said Lindsay Owens, executive director of Groundwork Collabortive Action.

"If Republicans want to talk about deficit reduction," Owens added, "Democrats have an easy response: Let's make the wealthiest Americans and biggest corporations pay their fair share before asking workers and families to pay a penny more."

"The Treasury Department can and should exercise the full extent of its regulatory authority to limit this blatant abuse of our tax system by the ultrawealthy."

Four U.S senators this week called on Treasury Secretary Janet Yellen to use her existing authority to go after American billionaires and multimillionaires who "use trusts to shift wealth to their heirs tax-free, dodging federal estate and gift taxes."

"They are doing this in the open: Their wealth managers are bragging about how their tax dodging tricks will be more effective in the current economy," stressed Sens. Elizabeth Warren (D-Mass.), Chris Van Hollen (D-Md.), Bernie Sanders (I-Vt.), and Sheldon Whitehouse (D-R.I.).

"While we look forward to continuing to partner with you on legislative solutions," the senators wrote to Yellen, "the Treasury Department can and should exercise the full extent of its regulatory authority to limit this blatant abuse of our tax system by the ultrawealthy."

Their letter to the Treasury leader, dated Monday and first reported by CBS MoneyWatch Tuesday, highlights that "only the wealthiest American families" are asked to pay transfer taxes such as the estate tax, gift tax, and generation-skipping transfer (GST) tax.

As the letter lays out:

Tax avoidance through grantor trusts starts with the ultrawealthy putting assets into a trust with the intention of transferring them to heirs. Grantor trusts are trusts where the grantor retains control over the assets, and the structures of some of these grantor trusts allow the transfer of massive sums tax-free. Tax planning via grantor trusts, including grantor retained annuity trusts (GRATs), is a kind of shell game, with a wealthy person and their wealth managers able to pass assets back and forth in ways that effectively pass wealth to heirs while minimizing tax liability.

Some of the wealthiest families further compound this tax avoidance with perpetual dynasty trusts, which can be used to shield assets from transfer tax liability indefinitely. For example, aggressive valuation discounts can artificially reduce the value of assets transferred into a trust below the GST tax exemption threshold, after which the assets can grow in perpetuity within a trust exempt from transfer tax.

"The ultrawealthy at the top of the socioeconomic ladder live by different rules than the rest of America, especially when it comes to our tax system," the letter charges. "As the richest Americans celebrate and take advantage of these favorable tax opportunities, middle-class families struggle with inflation and Republicans threaten austerity measures and the end of Social Security and Medicare."

To help force the richest Americans to "pay their fair share" in taxes, the senators are calling on Treasury to revoke a pair of tax code rulings from the Internal Revenue Service (IRS); require GRATs to have a minimum remainder value; reissue family limited partnership regulations; clarify that intentionally defective grantor trusts (IDGTs) are not entitled to stepped-up basis; and put out clarifying regulations on certain valuation rules for estate and gift taxes.

The senators also sent a series of questions—about potential administrative action, how much is estimated to be held in grantor trusts, and how much could be raised from cracking down on abuse—and requested a response from Treasury by April 3.

Their letter comes after President Joe Biden earlier this month introduced a budget blueprint for fiscal year 2024 that would hike taxes on the rich—proposed policies praised by progressive experts and advocates as "fair, popular, and long overdue."

Yellen last week appeared before the Senate Finance Committee—of which Warren and Whitehouse are members—to testify about the administration's proposal. She said in part that "our proposed budget builds on our economic progress by making smart, fiscally responsible investments. These investments would be more than fully paid for by requiring corporations and the wealthiest to pay their fair share."

"If we can provide over a trillion dollars in tax breaks to the top 1 percent and large corporations," said Senator Bernie Sanders this week, "please don't tell me that we cannot afford to make sure that every teacher in America is paid at least $60,000 a year."

How can we measure the work a particular society truly values? Take-home pay can make as good a yardstick as any: The lower an occupation’s compensation, the lower the esteem a society is showing for that occupation.

In the United States, our pay data show, no profession faces a reality that makes this link plainer — and uglier — than teaching.

All sorts of metrics can help us measure the level of our society’s esteem for the teaching profession. Are young people, for instance, interested in becoming teachers? Between 2008 and 2019, teacher ed enrollments in the United States plunged by over a third. Are current teachers feeling valued? Between 2019 and 2022, teacher retirements and resignations rose 40 percent.

But nothing says “esteem” more directly than paychecks, and, by that metric, American society has for years been systematically devaluing the work teachers do. Between 1996 and 2021, the Economic Policy Institute’s Sylvia Allegretto detailed last August, average teacher weekly wages adjusted for inflation rose a miniscule $29. Over the same years, inflation-adjusted weekly wages for other college graduates rose over 15 times faster, up $445.

What has this shortfall in overall compensation and esteem meant for America’s schools? In the current school year, the U.S. Department of Education reports, every single state in the union has reported teacher shortages, with 46 states citing shortages of science teachers and 44 missing math teachers.

Overall, some 36,000 teaching positions nationwide are going vacant, with at least 163,000 additional positions getting “filled” with unqualified teachers. Both these numbers, concludes a study by researchers at Brown University’s Annenberg Institute, represent “conservative estimates of the extent of teacher shortages nationally.”

Some observers of our contemporary education scene are contending, Stanford’s Linda Darling-Hammond noted last month, that the teacher resignations and vacancies we’re experiencing shouldn’t particularly concern us because they appear mostly in certain subjects and parts of the country. But that amounts to arguing, Darling-Hammond observes, that a house isn’t on fire “because only three of its five rooms are burning.”

Our educational house most definitely is burning, U.S. Senator Bernie Sanders told a town hall on America’s teacher pay crisis at the U.S. Capitol earlier this week.

“I want the day to come, sooner than later, when we are going to attract the best and brightest young people in our country into teaching,” said Sanders. “I want those young people to be proud of the profession that they have chosen.”

All teachers, the Vermont senator believes, should be earning at least $60,000 a year. Some 43 percent of teachers currently fall short of that mark. In Florida, the average teacher earns less than $50,000, just $49,583.

How do the bargain-basement paychecks that go to teachers compare with compensation for other professions? Not well at all. In Florida, accountants make $76,320 annually, 54 percent more than teachers. And software developers in Florida average $105,200, 112 percent more.

But the most stunning pay contrasts show up when we contrast teacher pay to the compensation of our nation’s most generously rewarded power suits.

“The top 15 hedge fund managers on Wall Street,” notes Senator Sanders, “make more money in a single year than every kindergarten teacher in America — over 120,000 teachers.”

Sanders will soon be introducing legislation, the Pay Teachers Act, to ensure that all teachers make at least $60,000 annually and guarantee significantly higher pay for educators “who have made teaching their profession — working on the job for 10, 20, 30 years.”

Where could the funding for this teacher pay revolution come from? From a tax revolution.

Public schools across the nation have historically relied on the local property taxes that average Americans pay. Property taxes today are still supplying 40 percent of total public education funding. These taxes all fall on the primary source of wealth for average families, the owner-occupied home. But America’s rich hold most of their wealth in financial instruments, a category of wealth that essentially goes untaxed, even after death, since the current federal estate tax asks so little from families sitting on grand fortunes.

Senator Sanders has proposed a fix: a thorough-going reform of the federal estate tax. Rich married couples last year could exempt $23.4 million of their fortunes from all estate tax and pay no more than a 40 percent tax on any dollar of wealth above that. The Sanders legislation — the “For the 99.5 Percent Act” — would lower that estate tax exemption to $7 million per married couple and up the minimal estate tax rate on wealth above that level to 45 percent.

Wealthier estates would face even higher rates, with wealth over $1 billion facing a 65 percent estate tax.

The Sanders legislation also takes aim at current loopholes that lower the rate of estate tax that the families of dead deep pockets actually face. Over his legislation’s first 10 years, Senator Sanders notes, the federal treasury would collect an additional $450 billion in estate tax revenue, “precisely how much the Teacher Pay Act would cost.”

“Let’s be clear,” the senator added at the U.S. Capitol teacher pay town hall Monday. “If we can provide over a trillion dollars in tax breaks to the top 1 percent and large corporations, please don’t tell me that we cannot afford to make sure that every teacher in America is paid at least $60,000 a year.”