SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

U.S. President Donald Trump (C), first lady Melania Trump, their son Barron, National Turkey Federation Chairman Carl Wittenburg and his family and members of the Draper County, Minnesota, 4-H chapater pose for photographs after Trump pardoned, Drumstick, the National Thanksgiving Turkey in the Rose Garden at the White House November 21, 2017 in Washington, DC. (Photo: Chip Somodevilla/Getty Images)

In recent years we've used the tradition of arguing with cranky relatives over the holidays to arm people with evidence to bat back silly economic arguments that are made all year long. This year, most dinner table arguments will likely be about Roy Moore, Al Franken, and maybe Russia, and on those, well, you're on your own.

But if debates do stray to economics, the topic is likely to be the tax bill being pushed by Republicans in Congress and the White House. If this bill becomes law, it would be a terrible shame. But until it does, the debate surrounding it is actually useful. It is by far the clearest sign that the Trump administration, while chaotic and unprecedented in many ways, is utterly conventional when it comes to making economic policy. The highest priority of Republicans in Congress in recent decades has been slashing taxes for rich households and corporations, and the Trump administration has thrown in completely with this effort.

"The highest priority of Republicans in Congress in recent decades has been slashing taxes for rich households and corporations, and the Trump administration has thrown in completely with this effort."

The centerpieces of the bills passed by the House and voted out of the Senate Finance committee last week are large tax cuts for businesses, both corporate and non-corporate. The corporate rate cuts are by far the largest parts of both bills, and the corporate changes are the only parts of the Senate bill that remain permanent--almost all of the changes to the individual code phase out in 2025. Non-corporate businesses--or "pass-throughs"--receive very large cuts in both bills, but because pass-through income is taxed on individual tax returns rather than at the business level, these changes expire in the Senate bill in 2025, along with most other individual changes.

There are lots of changes to individual, non-business taxes, for sure, but the net effect of these changes are much smaller than the business tax cuts, both in terms of overall cost and distribution, with some typical families seeing tax cuts and others seeing tax increases. Notably, however, the only individual changes in the Senate bill remaining after 2025 will leave most taxpayers facing slightly higher tax rates. All in all, these bills are mostly about slashing taxes for businesses, and particularly corporations.

Why cut taxes on businesses, particularly corporations? Because such cuts provide huge benefits to the top 1 percent. In fact, business income--both corporate and non-corporate--is among the most unequally distributed types of income in the economy. These tax cuts will be a windfall to business owners and owners of corporate stock, including the CEOs who manage these companies and get paid with stock. Nobody disagrees with this assessment.

The Republican marketing strategy has been to claim that while this is the first-round effect of business tax cuts, these cuts will then set off a complex chain reaction wherein businesses use their windfall to make new productivity-enhancing investments, leading higher wages for American workers. There are chapters in economics textbooks that somewhat support this reasoning, but other chapters provide reasons why this might not occur. Most importantly by far, however, is what the real-world evidence tells us: there is nothing in recent American economic history, or in the recent history of international comparisons, or in the recent history of individual U.S. states that supports the claims that corporate tax cuts will lead to higher wages for American workers. Recent reactions from business leaders back this up: they are hard pressed to answer questions about how they'd actually increase investment in response to the tax cut.

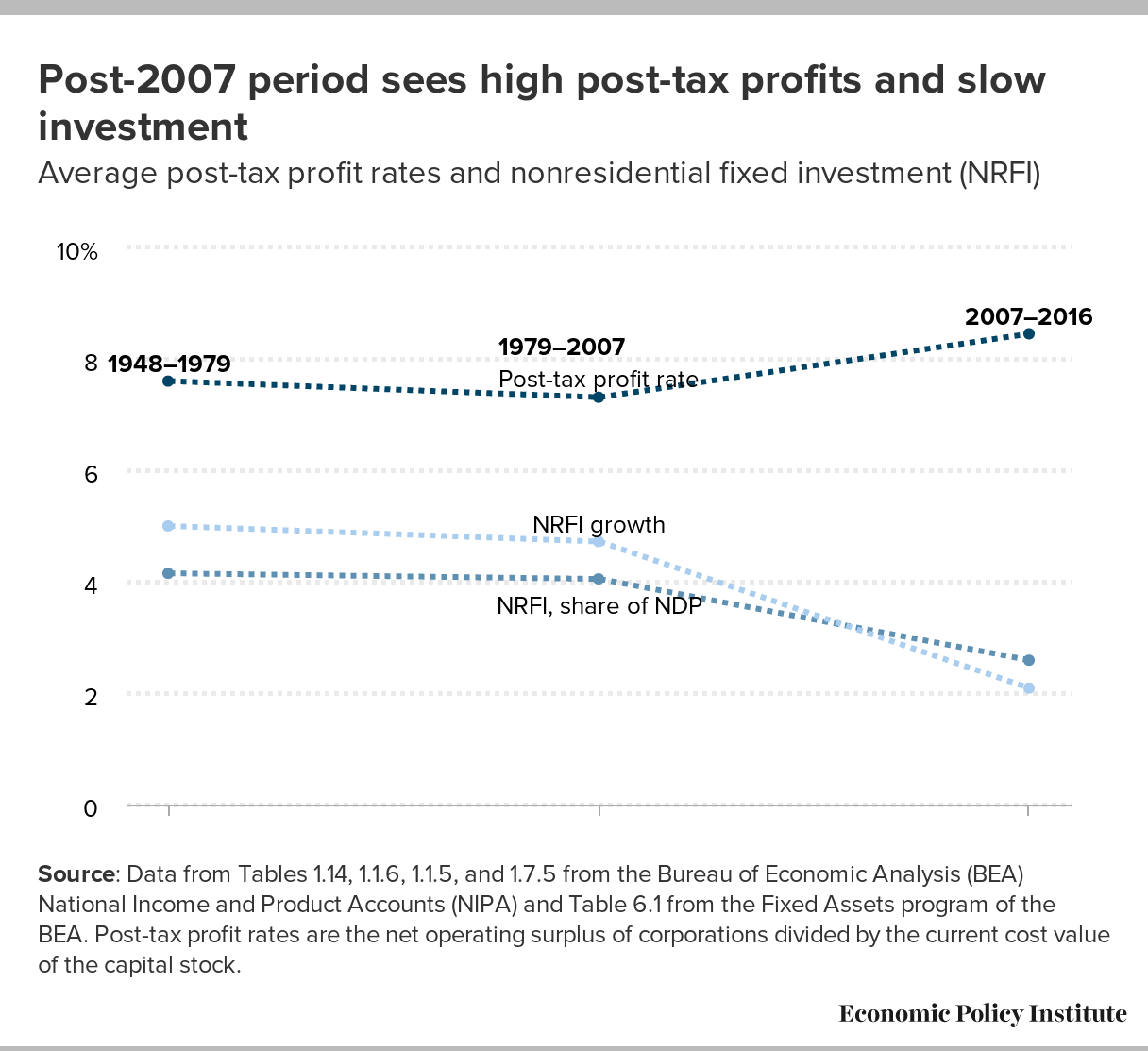

Perhaps the most intuitive reason why we know these cuts will fail to spark wage growth is that corporate profit rates have been historically high since 2007, while business investment has been historically low. Further, this has happened even while interest rates have been historically low, which should be providing an extra spur to this investment. So, if historically-high profit rates haven't generated productivity-enhancing investments over the past decade, why should we think that goosing these post-tax profit rates with tax cuts will all of the sudden make this investment appear?

Besides corporate tax cuts, the most damaging provisions of these bills are the way they treat "pass-through" income. The House bill caps the top tax rate on income from pass-through businesses at 25 percent. The Senate bill provides a slightly more complicated deduction that results in a similarly preferential rate, and in the Senate bill this preferential rate expires in 2025.

Most businesses aren't corporations, and so they aren't required to pay any income taxes at the business level. Instead, business owners pay taxes on their individual tax returns when the profits from their business are, yes, passed through to them. Republicans call capping the tax paid on pass-through income a "small business" tax cut. It's not. To understand why it's not, just remember that while all small businesses are pass-throughs, not all pass-throughs are small businesses. Some pass-throughs are hedge funds, or private equity firms, or mammoth real estate developers (Trump businesses are in fact pass-throughs).

The vast majority of genuine small businesses already face federal income tax rates of less than 25 percent, so they will gain no benefit from this 25 percent cap. Recent estimates from the U.S. Treasury indicate that pass-through income is actually more concentrated than corporate income is, with the top 1 percent claiming just under 70 percent of it. This means that if you agree that cutting taxes for corporations is providing a too generous benefit to the already affluent (i.e., the owners of these corporations), then you need to recognize that the Republican plan to lower taxes on pass-through income is even worse on this front.

If policymakers were sincere about wanting to cut some taxes to boost workers' wages, there are taxes they could cut that all economists agree would lead to higher pay for workers. The most direct one is payroll taxes. A cut in payroll taxes would before too long lead to higher wages. One complication is that payroll taxes are mostly earmarked to finance valuable social insurance programs like Social Security, Medicare, and unemployment insurance, so any plan to cut them would have to be accompanied by ironclad guarantees that these programs will be fully funded (say with earmarked funds out of other taxes, including general revenue). But such ironclad accounting would still be less complex than the bells and whistles accompanying current Republican plans to cut business taxes.

In the end, solving the problem of anemic wage growth for American workers will require looking to policies besides taxes. The broad middle class in America has seen steep declines in effective federal tax rates over the past generation of economic life, yet their pay has lagged far behind overall economic growth. As we have put it in the past, the problem with American paychecks isn't what taxes are taking out of them, it's what employers are failing to put in them.

To boost wage growth, policies that restore some genuine leverage to workers when they bargain with employers over pay need to be implemented. Key examples of policies that increase this leverage include ensuring the economy is pinned at very low rates of unemployment for extended periods of time and ensuring that the right of workers to bargain collectively is enforced. But there are literally dozens of other policies that would improve workers' leverage along important margins as well.

Finally, a plea when arguing with conservatives (or anybody else) about these tax cuts: no fear mongering over deficits. Are people who wring their hands over federal debt when Democrats are in charge complete hypocrites for pushing tax cuts today? Of course. And are deficits (inflated by tax cuts) often invoked as the need to savage Social Security, Medicare, Medicaid and the Affordable Care Act, and wouldn't gutting these programs be terrible for vulnerable Americans? Yes and yes. But there is no pressing economic reason to worry about federal budget deficits, and their political effectiveness as cudgels against Social Security, Medicare, Medicaid, and the ACA is only enhanced by well-meaning people echoing false claims supporting hysteria about debt.

The reason to oppose the latest round of Republican tax cuts is that they're simply unfair and stupid and solve no economic problem facing typical American families. That should be more than enough.

Dear Common Dreams reader, It’s been nearly 30 years since I co-founded Common Dreams with my late wife, Lina Newhouser. We had the radical notion that journalism should serve the public good, not corporate profits. It was clear to us from the outset what it would take to build such a project. No paid advertisements. No corporate sponsors. No millionaire publisher telling us what to think or do. Many people said we wouldn't last a year, but we proved those doubters wrong. Together with a tremendous team of journalists and dedicated staff, we built an independent media outlet free from the constraints of profits and corporate control. Our mission has always been simple: To inform. To inspire. To ignite change for the common good. Building Common Dreams was not easy. Our survival was never guaranteed. When you take on the most powerful forces—Wall Street greed, fossil fuel industry destruction, Big Tech lobbyists, and uber-rich oligarchs who have spent billions upon billions rigging the economy and democracy in their favor—the only bulwark you have is supporters who believe in your work. But here’s the urgent message from me today. It's never been this bad out there. And it's never been this hard to keep us going. At the very moment Common Dreams is most needed, the threats we face are intensifying. We need your support now more than ever. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. When everyone does the little they can afford, we are strong. But if that support retreats or dries up, so do we. Will you donate now to make sure Common Dreams not only survives but thrives? —Craig Brown, Co-founder |

In recent years we've used the tradition of arguing with cranky relatives over the holidays to arm people with evidence to bat back silly economic arguments that are made all year long. This year, most dinner table arguments will likely be about Roy Moore, Al Franken, and maybe Russia, and on those, well, you're on your own.

But if debates do stray to economics, the topic is likely to be the tax bill being pushed by Republicans in Congress and the White House. If this bill becomes law, it would be a terrible shame. But until it does, the debate surrounding it is actually useful. It is by far the clearest sign that the Trump administration, while chaotic and unprecedented in many ways, is utterly conventional when it comes to making economic policy. The highest priority of Republicans in Congress in recent decades has been slashing taxes for rich households and corporations, and the Trump administration has thrown in completely with this effort.

"The highest priority of Republicans in Congress in recent decades has been slashing taxes for rich households and corporations, and the Trump administration has thrown in completely with this effort."

The centerpieces of the bills passed by the House and voted out of the Senate Finance committee last week are large tax cuts for businesses, both corporate and non-corporate. The corporate rate cuts are by far the largest parts of both bills, and the corporate changes are the only parts of the Senate bill that remain permanent--almost all of the changes to the individual code phase out in 2025. Non-corporate businesses--or "pass-throughs"--receive very large cuts in both bills, but because pass-through income is taxed on individual tax returns rather than at the business level, these changes expire in the Senate bill in 2025, along with most other individual changes.

There are lots of changes to individual, non-business taxes, for sure, but the net effect of these changes are much smaller than the business tax cuts, both in terms of overall cost and distribution, with some typical families seeing tax cuts and others seeing tax increases. Notably, however, the only individual changes in the Senate bill remaining after 2025 will leave most taxpayers facing slightly higher tax rates. All in all, these bills are mostly about slashing taxes for businesses, and particularly corporations.

Why cut taxes on businesses, particularly corporations? Because such cuts provide huge benefits to the top 1 percent. In fact, business income--both corporate and non-corporate--is among the most unequally distributed types of income in the economy. These tax cuts will be a windfall to business owners and owners of corporate stock, including the CEOs who manage these companies and get paid with stock. Nobody disagrees with this assessment.

The Republican marketing strategy has been to claim that while this is the first-round effect of business tax cuts, these cuts will then set off a complex chain reaction wherein businesses use their windfall to make new productivity-enhancing investments, leading higher wages for American workers. There are chapters in economics textbooks that somewhat support this reasoning, but other chapters provide reasons why this might not occur. Most importantly by far, however, is what the real-world evidence tells us: there is nothing in recent American economic history, or in the recent history of international comparisons, or in the recent history of individual U.S. states that supports the claims that corporate tax cuts will lead to higher wages for American workers. Recent reactions from business leaders back this up: they are hard pressed to answer questions about how they'd actually increase investment in response to the tax cut.

Perhaps the most intuitive reason why we know these cuts will fail to spark wage growth is that corporate profit rates have been historically high since 2007, while business investment has been historically low. Further, this has happened even while interest rates have been historically low, which should be providing an extra spur to this investment. So, if historically-high profit rates haven't generated productivity-enhancing investments over the past decade, why should we think that goosing these post-tax profit rates with tax cuts will all of the sudden make this investment appear?

Besides corporate tax cuts, the most damaging provisions of these bills are the way they treat "pass-through" income. The House bill caps the top tax rate on income from pass-through businesses at 25 percent. The Senate bill provides a slightly more complicated deduction that results in a similarly preferential rate, and in the Senate bill this preferential rate expires in 2025.

Most businesses aren't corporations, and so they aren't required to pay any income taxes at the business level. Instead, business owners pay taxes on their individual tax returns when the profits from their business are, yes, passed through to them. Republicans call capping the tax paid on pass-through income a "small business" tax cut. It's not. To understand why it's not, just remember that while all small businesses are pass-throughs, not all pass-throughs are small businesses. Some pass-throughs are hedge funds, or private equity firms, or mammoth real estate developers (Trump businesses are in fact pass-throughs).

The vast majority of genuine small businesses already face federal income tax rates of less than 25 percent, so they will gain no benefit from this 25 percent cap. Recent estimates from the U.S. Treasury indicate that pass-through income is actually more concentrated than corporate income is, with the top 1 percent claiming just under 70 percent of it. This means that if you agree that cutting taxes for corporations is providing a too generous benefit to the already affluent (i.e., the owners of these corporations), then you need to recognize that the Republican plan to lower taxes on pass-through income is even worse on this front.

If policymakers were sincere about wanting to cut some taxes to boost workers' wages, there are taxes they could cut that all economists agree would lead to higher pay for workers. The most direct one is payroll taxes. A cut in payroll taxes would before too long lead to higher wages. One complication is that payroll taxes are mostly earmarked to finance valuable social insurance programs like Social Security, Medicare, and unemployment insurance, so any plan to cut them would have to be accompanied by ironclad guarantees that these programs will be fully funded (say with earmarked funds out of other taxes, including general revenue). But such ironclad accounting would still be less complex than the bells and whistles accompanying current Republican plans to cut business taxes.

In the end, solving the problem of anemic wage growth for American workers will require looking to policies besides taxes. The broad middle class in America has seen steep declines in effective federal tax rates over the past generation of economic life, yet their pay has lagged far behind overall economic growth. As we have put it in the past, the problem with American paychecks isn't what taxes are taking out of them, it's what employers are failing to put in them.

To boost wage growth, policies that restore some genuine leverage to workers when they bargain with employers over pay need to be implemented. Key examples of policies that increase this leverage include ensuring the economy is pinned at very low rates of unemployment for extended periods of time and ensuring that the right of workers to bargain collectively is enforced. But there are literally dozens of other policies that would improve workers' leverage along important margins as well.

Finally, a plea when arguing with conservatives (or anybody else) about these tax cuts: no fear mongering over deficits. Are people who wring their hands over federal debt when Democrats are in charge complete hypocrites for pushing tax cuts today? Of course. And are deficits (inflated by tax cuts) often invoked as the need to savage Social Security, Medicare, Medicaid and the Affordable Care Act, and wouldn't gutting these programs be terrible for vulnerable Americans? Yes and yes. But there is no pressing economic reason to worry about federal budget deficits, and their political effectiveness as cudgels against Social Security, Medicare, Medicaid, and the ACA is only enhanced by well-meaning people echoing false claims supporting hysteria about debt.

The reason to oppose the latest round of Republican tax cuts is that they're simply unfair and stupid and solve no economic problem facing typical American families. That should be more than enough.

In recent years we've used the tradition of arguing with cranky relatives over the holidays to arm people with evidence to bat back silly economic arguments that are made all year long. This year, most dinner table arguments will likely be about Roy Moore, Al Franken, and maybe Russia, and on those, well, you're on your own.

But if debates do stray to economics, the topic is likely to be the tax bill being pushed by Republicans in Congress and the White House. If this bill becomes law, it would be a terrible shame. But until it does, the debate surrounding it is actually useful. It is by far the clearest sign that the Trump administration, while chaotic and unprecedented in many ways, is utterly conventional when it comes to making economic policy. The highest priority of Republicans in Congress in recent decades has been slashing taxes for rich households and corporations, and the Trump administration has thrown in completely with this effort.

"The highest priority of Republicans in Congress in recent decades has been slashing taxes for rich households and corporations, and the Trump administration has thrown in completely with this effort."

The centerpieces of the bills passed by the House and voted out of the Senate Finance committee last week are large tax cuts for businesses, both corporate and non-corporate. The corporate rate cuts are by far the largest parts of both bills, and the corporate changes are the only parts of the Senate bill that remain permanent--almost all of the changes to the individual code phase out in 2025. Non-corporate businesses--or "pass-throughs"--receive very large cuts in both bills, but because pass-through income is taxed on individual tax returns rather than at the business level, these changes expire in the Senate bill in 2025, along with most other individual changes.

There are lots of changes to individual, non-business taxes, for sure, but the net effect of these changes are much smaller than the business tax cuts, both in terms of overall cost and distribution, with some typical families seeing tax cuts and others seeing tax increases. Notably, however, the only individual changes in the Senate bill remaining after 2025 will leave most taxpayers facing slightly higher tax rates. All in all, these bills are mostly about slashing taxes for businesses, and particularly corporations.

Why cut taxes on businesses, particularly corporations? Because such cuts provide huge benefits to the top 1 percent. In fact, business income--both corporate and non-corporate--is among the most unequally distributed types of income in the economy. These tax cuts will be a windfall to business owners and owners of corporate stock, including the CEOs who manage these companies and get paid with stock. Nobody disagrees with this assessment.

The Republican marketing strategy has been to claim that while this is the first-round effect of business tax cuts, these cuts will then set off a complex chain reaction wherein businesses use their windfall to make new productivity-enhancing investments, leading higher wages for American workers. There are chapters in economics textbooks that somewhat support this reasoning, but other chapters provide reasons why this might not occur. Most importantly by far, however, is what the real-world evidence tells us: there is nothing in recent American economic history, or in the recent history of international comparisons, or in the recent history of individual U.S. states that supports the claims that corporate tax cuts will lead to higher wages for American workers. Recent reactions from business leaders back this up: they are hard pressed to answer questions about how they'd actually increase investment in response to the tax cut.

Perhaps the most intuitive reason why we know these cuts will fail to spark wage growth is that corporate profit rates have been historically high since 2007, while business investment has been historically low. Further, this has happened even while interest rates have been historically low, which should be providing an extra spur to this investment. So, if historically-high profit rates haven't generated productivity-enhancing investments over the past decade, why should we think that goosing these post-tax profit rates with tax cuts will all of the sudden make this investment appear?

Besides corporate tax cuts, the most damaging provisions of these bills are the way they treat "pass-through" income. The House bill caps the top tax rate on income from pass-through businesses at 25 percent. The Senate bill provides a slightly more complicated deduction that results in a similarly preferential rate, and in the Senate bill this preferential rate expires in 2025.

Most businesses aren't corporations, and so they aren't required to pay any income taxes at the business level. Instead, business owners pay taxes on their individual tax returns when the profits from their business are, yes, passed through to them. Republicans call capping the tax paid on pass-through income a "small business" tax cut. It's not. To understand why it's not, just remember that while all small businesses are pass-throughs, not all pass-throughs are small businesses. Some pass-throughs are hedge funds, or private equity firms, or mammoth real estate developers (Trump businesses are in fact pass-throughs).

The vast majority of genuine small businesses already face federal income tax rates of less than 25 percent, so they will gain no benefit from this 25 percent cap. Recent estimates from the U.S. Treasury indicate that pass-through income is actually more concentrated than corporate income is, with the top 1 percent claiming just under 70 percent of it. This means that if you agree that cutting taxes for corporations is providing a too generous benefit to the already affluent (i.e., the owners of these corporations), then you need to recognize that the Republican plan to lower taxes on pass-through income is even worse on this front.

If policymakers were sincere about wanting to cut some taxes to boost workers' wages, there are taxes they could cut that all economists agree would lead to higher pay for workers. The most direct one is payroll taxes. A cut in payroll taxes would before too long lead to higher wages. One complication is that payroll taxes are mostly earmarked to finance valuable social insurance programs like Social Security, Medicare, and unemployment insurance, so any plan to cut them would have to be accompanied by ironclad guarantees that these programs will be fully funded (say with earmarked funds out of other taxes, including general revenue). But such ironclad accounting would still be less complex than the bells and whistles accompanying current Republican plans to cut business taxes.

In the end, solving the problem of anemic wage growth for American workers will require looking to policies besides taxes. The broad middle class in America has seen steep declines in effective federal tax rates over the past generation of economic life, yet their pay has lagged far behind overall economic growth. As we have put it in the past, the problem with American paychecks isn't what taxes are taking out of them, it's what employers are failing to put in them.

To boost wage growth, policies that restore some genuine leverage to workers when they bargain with employers over pay need to be implemented. Key examples of policies that increase this leverage include ensuring the economy is pinned at very low rates of unemployment for extended periods of time and ensuring that the right of workers to bargain collectively is enforced. But there are literally dozens of other policies that would improve workers' leverage along important margins as well.

Finally, a plea when arguing with conservatives (or anybody else) about these tax cuts: no fear mongering over deficits. Are people who wring their hands over federal debt when Democrats are in charge complete hypocrites for pushing tax cuts today? Of course. And are deficits (inflated by tax cuts) often invoked as the need to savage Social Security, Medicare, Medicaid and the Affordable Care Act, and wouldn't gutting these programs be terrible for vulnerable Americans? Yes and yes. But there is no pressing economic reason to worry about federal budget deficits, and their political effectiveness as cudgels against Social Security, Medicare, Medicaid, and the ACA is only enhanced by well-meaning people echoing false claims supporting hysteria about debt.

The reason to oppose the latest round of Republican tax cuts is that they're simply unfair and stupid and solve no economic problem facing typical American families. That should be more than enough.

{kind=link}

{kind=link}

{kind=link}