SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

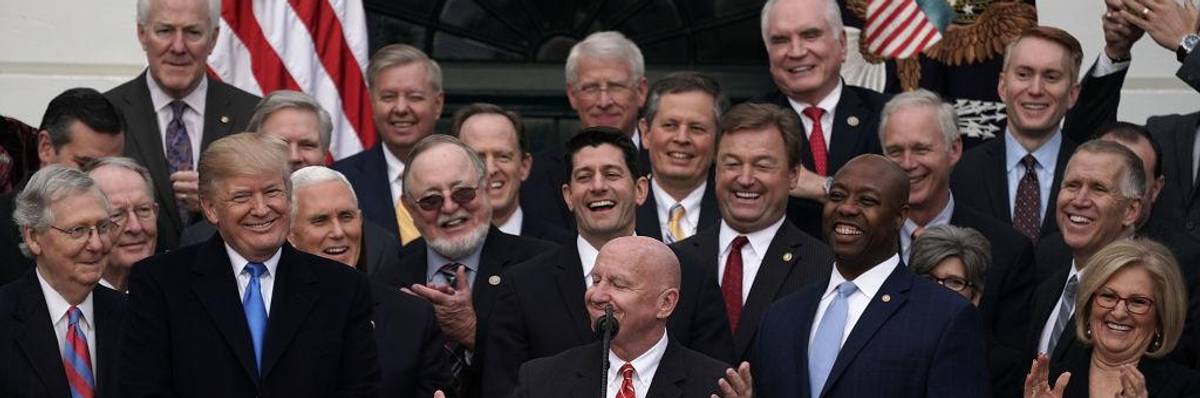

Chairman of House Ways and Means Committee Rep. Kevin Brady (R-TX) (C) as President Donald Trump (3rd L) looks on during an event to celebrate Congress passing the Tax Cuts and Jobs Act with Republican members of the House and Senate on the South Lawn of the White House December 20, 2017 in Washington, DC. The tax bill is the first major legislative victory for the GOP-controlled Congress and Trump since he took office almost one year ago.

The share of these companies who paid zero in federal income tax rose from 22 percent in 2014 to 34 percent in 2018, the first year that the Trump tax law was in effect.

The tax cuts signed into law by former President Trump at the end of 2017 were a boon for profitable corporations, according to a new report released by the Government Accountability Office. It finds the average effective federal income tax rate paid by large, profitable corporations fell to 9 percent in the first year that the Trump tax law was in effect, and the share of such companies paying nothing at all rose to 34 percent that year.

This is consistent with our findings that profitable corporations often pay little or nothing. While the corporate minimum tax passed this summer will help, Congress now needs to pass the international corporate minimum tax to further address this problem.

The GAO analysis presents many different types of figures, but all show the Tax Cuts and Jobs Act was an unprecedented gift to corporations. For example, it finds that the share of all corporations paying no federal income taxes was 67 percent in 2018 and had not changed much over the years. But that is not so surprising because that figure includes tiny companies and companies reporting losses, which are not expected to pay income taxes. (The federal corporate income tax is, after all, a tax on profits, not losses).

Much more alarming are the GAO’s conclusions about corporations that are both large (which GAO defines as having at least $10 million in assets) and profitable. The share of these companies paying nothing rose from 22 percent in 2014 to 34 percent in 2018, the first year that the Trump tax law was in effect.

What the GAO report really demonstrates is that no matter how you measure the federal corporate income tax, not much of it has been paid in recent years, and the 2017 tax law has brought it to a new low.

The average effective federal income tax rate paid by these companies (the share of profits they paid in federal income taxes) fell from an already-low 16 percent in 2014 to a nearly rock-bottom-low 9 percent in 2018.

These estimates use corporations’ actual tax liability based on IRS data that is not available to researchers outside the government. Still, the GAO report shows that the “current” tax reported by publicly traded corporations in the filings they submit to the Securities and Exchange Commission (which is what ITEP uses to identify how much specific corporations pay) comes to roughly the same answers.

For example, while GAO found that average effective tax rates based on actual tax liability (using IRS data) fell from 16 percent in 2014 to 9 percent in 2018, an alternative version of those figures calculated using current taxes reported in the public filings are just a bit different, at 17 percent in 2014 and 8 percent in 2018.

Even profitable corporations might pay nothing in one year because they are allowed to carry forward losses from previous years. If the system works as intended, corporations that are profitable in the long run will pay taxes at a reasonable effective rate over time. But the GAO analysis demonstrates that even if the data is adjusted to ignore the deductions that companies can claim for losses, the conclusions do not change very much (in which case the average effective income tax rates increase slightly to 18 percent in 2014 and 10 percent in 2018). This is unsurprising because ITEP has followed corporations that were profitable each year for several years in a row and found that even these fortunate companies often manage to pay nothing over time.

What the GAO report really demonstrates is that no matter how you measure the federal corporate income tax, not much of it has been paid in recent years, and the 2017 tax law has brought it to a new low.

The corporate minimum tax enacted as part of the Inflation Reduction Act will help address this problem. But as ITEP has explained, another key step for Congress is to implement the international corporate minimum tax that the Biden administration negotiated with other governments, and which is designed to address the offshore tax dodging that will otherwise be very difficult to resolve.

Dear Common Dreams reader, It’s been nearly 30 years since I co-founded Common Dreams with my late wife, Lina Newhouser. We had the radical notion that journalism should serve the public good, not corporate profits. It was clear to us from the outset what it would take to build such a project. No paid advertisements. No corporate sponsors. No millionaire publisher telling us what to think or do. Many people said we wouldn't last a year, but we proved those doubters wrong. Together with a tremendous team of journalists and dedicated staff, we built an independent media outlet free from the constraints of profits and corporate control. Our mission has always been simple: To inform. To inspire. To ignite change for the common good. Building Common Dreams was not easy. Our survival was never guaranteed. When you take on the most powerful forces—Wall Street greed, fossil fuel industry destruction, Big Tech lobbyists, and uber-rich oligarchs who have spent billions upon billions rigging the economy and democracy in their favor—the only bulwark you have is supporters who believe in your work. But here’s the urgent message from me today. It's never been this bad out there. And it's never been this hard to keep us going. At the very moment Common Dreams is most needed, the threats we face are intensifying. We need your support now more than ever. We don't accept corporate advertising and never will. We don't have a paywall because we don't think people should be blocked from critical news based on their ability to pay. Everything we do is funded by the donations of readers like you. When everyone does the little they can afford, we are strong. But if that support retreats or dries up, so do we. Will you donate now to make sure Common Dreams not only survives but thrives? —Craig Brown, Co-founder |

The tax cuts signed into law by former President Trump at the end of 2017 were a boon for profitable corporations, according to a new report released by the Government Accountability Office. It finds the average effective federal income tax rate paid by large, profitable corporations fell to 9 percent in the first year that the Trump tax law was in effect, and the share of such companies paying nothing at all rose to 34 percent that year.

This is consistent with our findings that profitable corporations often pay little or nothing. While the corporate minimum tax passed this summer will help, Congress now needs to pass the international corporate minimum tax to further address this problem.

The GAO analysis presents many different types of figures, but all show the Tax Cuts and Jobs Act was an unprecedented gift to corporations. For example, it finds that the share of all corporations paying no federal income taxes was 67 percent in 2018 and had not changed much over the years. But that is not so surprising because that figure includes tiny companies and companies reporting losses, which are not expected to pay income taxes. (The federal corporate income tax is, after all, a tax on profits, not losses).

Much more alarming are the GAO’s conclusions about corporations that are both large (which GAO defines as having at least $10 million in assets) and profitable. The share of these companies paying nothing rose from 22 percent in 2014 to 34 percent in 2018, the first year that the Trump tax law was in effect.

What the GAO report really demonstrates is that no matter how you measure the federal corporate income tax, not much of it has been paid in recent years, and the 2017 tax law has brought it to a new low.

The average effective federal income tax rate paid by these companies (the share of profits they paid in federal income taxes) fell from an already-low 16 percent in 2014 to a nearly rock-bottom-low 9 percent in 2018.

These estimates use corporations’ actual tax liability based on IRS data that is not available to researchers outside the government. Still, the GAO report shows that the “current” tax reported by publicly traded corporations in the filings they submit to the Securities and Exchange Commission (which is what ITEP uses to identify how much specific corporations pay) comes to roughly the same answers.

For example, while GAO found that average effective tax rates based on actual tax liability (using IRS data) fell from 16 percent in 2014 to 9 percent in 2018, an alternative version of those figures calculated using current taxes reported in the public filings are just a bit different, at 17 percent in 2014 and 8 percent in 2018.

Even profitable corporations might pay nothing in one year because they are allowed to carry forward losses from previous years. If the system works as intended, corporations that are profitable in the long run will pay taxes at a reasonable effective rate over time. But the GAO analysis demonstrates that even if the data is adjusted to ignore the deductions that companies can claim for losses, the conclusions do not change very much (in which case the average effective income tax rates increase slightly to 18 percent in 2014 and 10 percent in 2018). This is unsurprising because ITEP has followed corporations that were profitable each year for several years in a row and found that even these fortunate companies often manage to pay nothing over time.

What the GAO report really demonstrates is that no matter how you measure the federal corporate income tax, not much of it has been paid in recent years, and the 2017 tax law has brought it to a new low.

The corporate minimum tax enacted as part of the Inflation Reduction Act will help address this problem. But as ITEP has explained, another key step for Congress is to implement the international corporate minimum tax that the Biden administration negotiated with other governments, and which is designed to address the offshore tax dodging that will otherwise be very difficult to resolve.

The tax cuts signed into law by former President Trump at the end of 2017 were a boon for profitable corporations, according to a new report released by the Government Accountability Office. It finds the average effective federal income tax rate paid by large, profitable corporations fell to 9 percent in the first year that the Trump tax law was in effect, and the share of such companies paying nothing at all rose to 34 percent that year.

This is consistent with our findings that profitable corporations often pay little or nothing. While the corporate minimum tax passed this summer will help, Congress now needs to pass the international corporate minimum tax to further address this problem.

The GAO analysis presents many different types of figures, but all show the Tax Cuts and Jobs Act was an unprecedented gift to corporations. For example, it finds that the share of all corporations paying no federal income taxes was 67 percent in 2018 and had not changed much over the years. But that is not so surprising because that figure includes tiny companies and companies reporting losses, which are not expected to pay income taxes. (The federal corporate income tax is, after all, a tax on profits, not losses).

Much more alarming are the GAO’s conclusions about corporations that are both large (which GAO defines as having at least $10 million in assets) and profitable. The share of these companies paying nothing rose from 22 percent in 2014 to 34 percent in 2018, the first year that the Trump tax law was in effect.

What the GAO report really demonstrates is that no matter how you measure the federal corporate income tax, not much of it has been paid in recent years, and the 2017 tax law has brought it to a new low.

The average effective federal income tax rate paid by these companies (the share of profits they paid in federal income taxes) fell from an already-low 16 percent in 2014 to a nearly rock-bottom-low 9 percent in 2018.

These estimates use corporations’ actual tax liability based on IRS data that is not available to researchers outside the government. Still, the GAO report shows that the “current” tax reported by publicly traded corporations in the filings they submit to the Securities and Exchange Commission (which is what ITEP uses to identify how much specific corporations pay) comes to roughly the same answers.

For example, while GAO found that average effective tax rates based on actual tax liability (using IRS data) fell from 16 percent in 2014 to 9 percent in 2018, an alternative version of those figures calculated using current taxes reported in the public filings are just a bit different, at 17 percent in 2014 and 8 percent in 2018.

Even profitable corporations might pay nothing in one year because they are allowed to carry forward losses from previous years. If the system works as intended, corporations that are profitable in the long run will pay taxes at a reasonable effective rate over time. But the GAO analysis demonstrates that even if the data is adjusted to ignore the deductions that companies can claim for losses, the conclusions do not change very much (in which case the average effective income tax rates increase slightly to 18 percent in 2014 and 10 percent in 2018). This is unsurprising because ITEP has followed corporations that were profitable each year for several years in a row and found that even these fortunate companies often manage to pay nothing over time.

What the GAO report really demonstrates is that no matter how you measure the federal corporate income tax, not much of it has been paid in recent years, and the 2017 tax law has brought it to a new low.

The corporate minimum tax enacted as part of the Inflation Reduction Act will help address this problem. But as ITEP has explained, another key step for Congress is to implement the international corporate minimum tax that the Biden administration negotiated with other governments, and which is designed to address the offshore tax dodging that will otherwise be very difficult to resolve.