5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

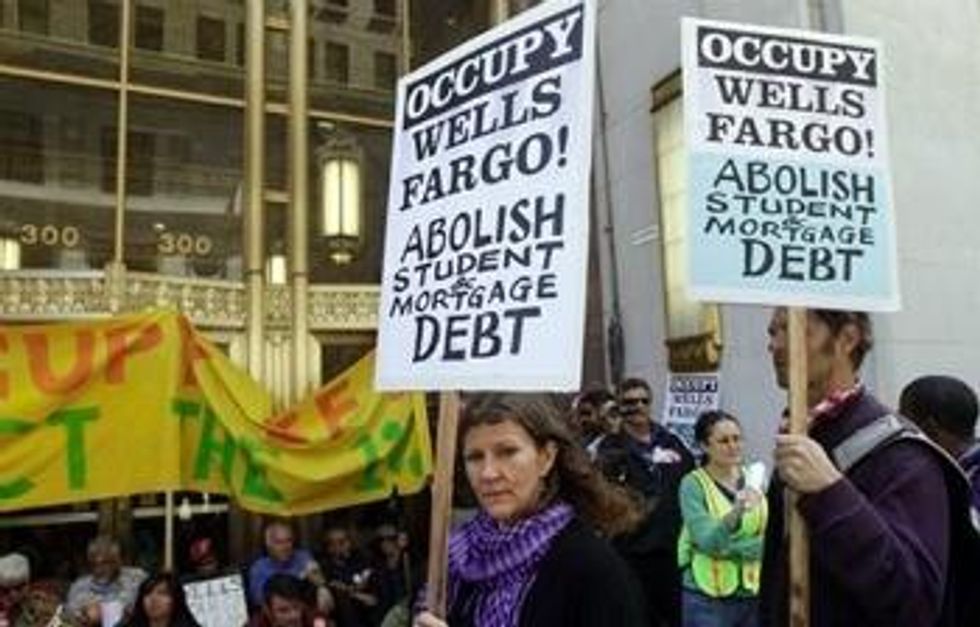

Inside and outside of Wells Fargo's annual meeting in San Francisco yesterday, thousands of angry protesters decried the bank's leading role in the loss of millions of American homes to foreclosure.

If you want to know why the protesters are so angry, consider this double standard. For most Americans, retirement security lies in the value of their homes. Millions of these people have been losing that security as the nation's largest banks have foreclosed on them. Yet the CEOs of these banks are reaping giant pay packages and padding their own retirement security with profits squeezed from ordinary people.

For many American families, a paid-off home is part of the dream of a secure retirement. The roof over their heads has long comprised the largest element of most families' net worth. The housing crisis brought to us by the country's biggest bankers has stolen the dreams of the nearly 4 million families who have lost their homes to foreclosure since the housing crisis began in 2007.

Of those who continue to live in their homes, more than a quarter have lost so much equity that they now owe more on their mortgage than their residence is worth. Even those who have never missed a payment on these underwater mortgages have found it all but impossible to refinance their loans to take advantage of record low rates that would cut hundreds of dollars from their monthly payments.

As American families struggle with their shrinking equity, Wells Fargo is enjoying record profits. Its earnings clocked in at more than $4 billion during the first quarter of 2012.

Wells Fargo and Bank of America are the country's two largest mortgage servicers. Over the past three years, the number of homes foreclosed upon by the two giant banks has steadily grown. At the end of 2011, they reported to federal banking regulators that they held $22.5 billion and $19 billion worth of foreclosed houses, respectively.

While foreclosures have devastated the financial security of millions of American families, the CEOs of Wells Fargo and Bank of America have seen their retirement packages balloon.

While foreclosures have devastated the financial security of millions of American families, the CEOs of Wells Fargo and Bank of America have seen their retirement packages balloon.

The pension assets of Wells Fargo CEO John Stumpf stand at $16 million, according to the company's proxy statement. The vast majority of these assets came from a special plan available only to the company's top executives. As high as Stumpf's retirement assets have soared, they're exceeded by those of another Wells Fargo executive. Mark Oman oversees the company's consumer lending division, where most of its ill-fated subprime loans were made and where many customers have lost their homes to foreclosure. His retirement assets top $17 million.

Bank of America CEO Brian Moynihan's pension assets now total $6.8 million. His nest egg came mainly from a special "supplemental" pension plan.

It's long past time that banking regulators stopped these dream-stealers from laughing their way to their gold-plated retirements. Protesters are insisting that the corporate funds diverted to prop up the lavish lifestyles of those responsible for upending the lives of the millions of American families who have lost their homes be redirected toward principal relief for homeowners devastated by these banks' actions.

The Wells Fargo action was just the start. Don't be surprised when thousands more protesters show up when Bank of America shareholders gather on May 9 in Charlotte, N.C.

Inside and outside of Wells Fargo's annual meeting in San Francisco yesterday, thousands of angry protesters decried the bank's leading role in the loss of millions of American homes to foreclosure.

If you want to know why the protesters are so angry, consider this double standard. For most Americans, retirement security lies in the value of their homes. Millions of these people have been losing that security as the nation's largest banks have foreclosed on them. Yet the CEOs of these banks are reaping giant pay packages and padding their own retirement security with profits squeezed from ordinary people.

For many American families, a paid-off home is part of the dream of a secure retirement. The roof over their heads has long comprised the largest element of most families' net worth. The housing crisis brought to us by the country's biggest bankers has stolen the dreams of the nearly 4 million families who have lost their homes to foreclosure since the housing crisis began in 2007.

Of those who continue to live in their homes, more than a quarter have lost so much equity that they now owe more on their mortgage than their residence is worth. Even those who have never missed a payment on these underwater mortgages have found it all but impossible to refinance their loans to take advantage of record low rates that would cut hundreds of dollars from their monthly payments.

As American families struggle with their shrinking equity, Wells Fargo is enjoying record profits. Its earnings clocked in at more than $4 billion during the first quarter of 2012.

Wells Fargo and Bank of America are the country's two largest mortgage servicers. Over the past three years, the number of homes foreclosed upon by the two giant banks has steadily grown. At the end of 2011, they reported to federal banking regulators that they held $22.5 billion and $19 billion worth of foreclosed houses, respectively.

While foreclosures have devastated the financial security of millions of American families, the CEOs of Wells Fargo and Bank of America have seen their retirement packages balloon.

While foreclosures have devastated the financial security of millions of American families, the CEOs of Wells Fargo and Bank of America have seen their retirement packages balloon.

The pension assets of Wells Fargo CEO John Stumpf stand at $16 million, according to the company's proxy statement. The vast majority of these assets came from a special plan available only to the company's top executives. As high as Stumpf's retirement assets have soared, they're exceeded by those of another Wells Fargo executive. Mark Oman oversees the company's consumer lending division, where most of its ill-fated subprime loans were made and where many customers have lost their homes to foreclosure. His retirement assets top $17 million.

Bank of America CEO Brian Moynihan's pension assets now total $6.8 million. His nest egg came mainly from a special "supplemental" pension plan.

It's long past time that banking regulators stopped these dream-stealers from laughing their way to their gold-plated retirements. Protesters are insisting that the corporate funds diverted to prop up the lavish lifestyles of those responsible for upending the lives of the millions of American families who have lost their homes be redirected toward principal relief for homeowners devastated by these banks' actions.

The Wells Fargo action was just the start. Don't be surprised when thousands more protesters show up when Bank of America shareholders gather on May 9 in Charlotte, N.C.

Inside and outside of Wells Fargo's annual meeting in San Francisco yesterday, thousands of angry protesters decried the bank's leading role in the loss of millions of American homes to foreclosure.

If you want to know why the protesters are so angry, consider this double standard. For most Americans, retirement security lies in the value of their homes. Millions of these people have been losing that security as the nation's largest banks have foreclosed on them. Yet the CEOs of these banks are reaping giant pay packages and padding their own retirement security with profits squeezed from ordinary people.

For many American families, a paid-off home is part of the dream of a secure retirement. The roof over their heads has long comprised the largest element of most families' net worth. The housing crisis brought to us by the country's biggest bankers has stolen the dreams of the nearly 4 million families who have lost their homes to foreclosure since the housing crisis began in 2007.

Of those who continue to live in their homes, more than a quarter have lost so much equity that they now owe more on their mortgage than their residence is worth. Even those who have never missed a payment on these underwater mortgages have found it all but impossible to refinance their loans to take advantage of record low rates that would cut hundreds of dollars from their monthly payments.

As American families struggle with their shrinking equity, Wells Fargo is enjoying record profits. Its earnings clocked in at more than $4 billion during the first quarter of 2012.

Wells Fargo and Bank of America are the country's two largest mortgage servicers. Over the past three years, the number of homes foreclosed upon by the two giant banks has steadily grown. At the end of 2011, they reported to federal banking regulators that they held $22.5 billion and $19 billion worth of foreclosed houses, respectively.

While foreclosures have devastated the financial security of millions of American families, the CEOs of Wells Fargo and Bank of America have seen their retirement packages balloon.

While foreclosures have devastated the financial security of millions of American families, the CEOs of Wells Fargo and Bank of America have seen their retirement packages balloon.

The pension assets of Wells Fargo CEO John Stumpf stand at $16 million, according to the company's proxy statement. The vast majority of these assets came from a special plan available only to the company's top executives. As high as Stumpf's retirement assets have soared, they're exceeded by those of another Wells Fargo executive. Mark Oman oversees the company's consumer lending division, where most of its ill-fated subprime loans were made and where many customers have lost their homes to foreclosure. His retirement assets top $17 million.

Bank of America CEO Brian Moynihan's pension assets now total $6.8 million. His nest egg came mainly from a special "supplemental" pension plan.

It's long past time that banking regulators stopped these dream-stealers from laughing their way to their gold-plated retirements. Protesters are insisting that the corporate funds diverted to prop up the lavish lifestyles of those responsible for upending the lives of the millions of American families who have lost their homes be redirected toward principal relief for homeowners devastated by these banks' actions.

The Wells Fargo action was just the start. Don't be surprised when thousands more protesters show up when Bank of America shareholders gather on May 9 in Charlotte, N.C.