SUBSCRIBE TO OUR FREE NEWSLETTER

Daily news & progressive opinion—funded by the people, not the corporations—delivered straight to your inbox.

5

#000000

#FFFFFF

To donate by check, phone, or other method, see our More Ways to Give page.

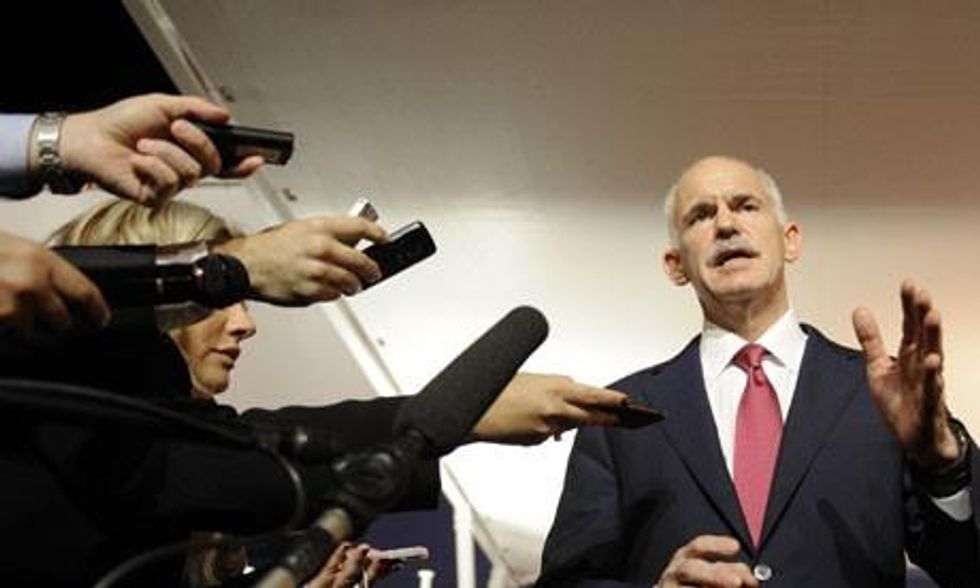

Greek Prime Minister George Papandreou touched off a firestorm last week when he proposed putting the austerity package designed by the "troika" (the IMF, the European Central Bank and the European Union) up for a popular vote. The idea that the Greek people might directly be able to decide their future terrified leaders across Europe and around the world. Financial markets panicked, sending stocks plummeting and bond yields soaring.

However, by the end of the week, things were back under control. The leaders of France and Germany apparently laid down the law to Papandreou and he backed off plans for the referendum. While the government is in the process of collapsing in Greece, the world can now rest assured that the Greek people will not have an opportunity to vote on their future.

This is unfortunate, since it means that Greece's future will likely be decided by politicians who may not have the interests of the Greek people foremost in their minds. By their own projections, the austerity package designed by the troika promises a decade of austerity, with high unemployment, falling real wages and sharp reductions in public services and pensions. And their projections have consistently proven to be overly optimistic.

If given the opportunity, would the Greek people endorse this sort of austerity package? The answer obviously depends on the alternative.

The alternative route almost certainly means a disorderly debt default and a departure from the euro. That is not a pretty picture. If Greece follows the path of Argentina, the last country to make a similar break, then the economy is likely to undergo a free fall for a period of time. The duration of this free fall will depend on how long it takes the government to get a new currency in use and construct some provisional formula for converting euro-denominated contracts into the new currency.

In Argentina, this period was three months, with another three months of stagnation before the economy began a sustained boom. The process could be more difficult in Greece, both because it is tied in more extensively to the eurozone countries, and because Argentina at least had its own currency.

However, even in the case of Greece, such a break would not be impossible. There would be a desire to hold the new currency. The government just has to impose a new property tax, which is only payable in the new currency.

People will want to hold onto ocean-front property in the Greek islands or at the foot of the Acropolis, so there will be demand for the currency. Also, the prospect of a tourist boom, once prices in Greece fall by 50% relative to Italy, Spain and other popular destinations will go a long towards supporting the Greek economy.

If the Greek people can convince themselves that this would be a plausible alternative, then they could make a few demands on the troika. First, they could say that ten years of continuous austerity is not acceptable.

Yes, the Greeks had been reckless borrowers, but the European banks had also been reckless lenders. It is true that the Greek government had lied about its budget situation. But the word among finance types is that everyone knew they were lying and went along with the joke. Goldman Sachs even designed a nifty swap that allowed it to profit from the lies.

Instead of austerity, the Greek people might insist that the ECB focus on a growth agenda. This would mean that the ECB would have to ditch its obsession with a 2% inflation target and start acting like a real central bank. The ECB could start by guaranteeing the debt of Italy and Spain, both of which risk a rising interest rate/debt default death spiral, if there is not a credible guarantee behind their debt.

It might also start pushing more expansionary policies. It's always hard to admit when you are wrong, but the ECB-IMF policy of growth through austerity is not working. Every month, we get more proof of this fact - with data showing that growth is lower than expected and unemployment is higher than expected. Is there any evidence that could get these people to change their minds before they destroy Europe's economies? Maybe, the Greek people could have forced the troika to actually look at the data.

There would have been other potential for fun in these negotiations. The Greek people, who have already been forced to accept a rise in their retirement age and lower pensions, may suggest the same for IMF economists. These hard-working types can often retire from their jobs in their early 50s. Instead of the meager Greek pensions of a few hundred euros a month that got the banker types so riled, the IMF crew can be pocketing close to $10,000 a month in their pensions. Perhaps IMF pensions would have come up for debate, if the Greek people actually had to be convinced that a bailout was in their own good.

But the chance to bring the Greek people into the discussion was quickly nixed. We are back to a conversation among the bankers and the politicians. There is not much room for democracy in this story, but we can still dream.

Greek Prime Minister George Papandreou touched off a firestorm last week when he proposed putting the austerity package designed by the "troika" (the IMF, the European Central Bank and the European Union) up for a popular vote. The idea that the Greek people might directly be able to decide their future terrified leaders across Europe and around the world. Financial markets panicked, sending stocks plummeting and bond yields soaring.

However, by the end of the week, things were back under control. The leaders of France and Germany apparently laid down the law to Papandreou and he backed off plans for the referendum. While the government is in the process of collapsing in Greece, the world can now rest assured that the Greek people will not have an opportunity to vote on their future.

This is unfortunate, since it means that Greece's future will likely be decided by politicians who may not have the interests of the Greek people foremost in their minds. By their own projections, the austerity package designed by the troika promises a decade of austerity, with high unemployment, falling real wages and sharp reductions in public services and pensions. And their projections have consistently proven to be overly optimistic.

If given the opportunity, would the Greek people endorse this sort of austerity package? The answer obviously depends on the alternative.

The alternative route almost certainly means a disorderly debt default and a departure from the euro. That is not a pretty picture. If Greece follows the path of Argentina, the last country to make a similar break, then the economy is likely to undergo a free fall for a period of time. The duration of this free fall will depend on how long it takes the government to get a new currency in use and construct some provisional formula for converting euro-denominated contracts into the new currency.

In Argentina, this period was three months, with another three months of stagnation before the economy began a sustained boom. The process could be more difficult in Greece, both because it is tied in more extensively to the eurozone countries, and because Argentina at least had its own currency.

However, even in the case of Greece, such a break would not be impossible. There would be a desire to hold the new currency. The government just has to impose a new property tax, which is only payable in the new currency.

People will want to hold onto ocean-front property in the Greek islands or at the foot of the Acropolis, so there will be demand for the currency. Also, the prospect of a tourist boom, once prices in Greece fall by 50% relative to Italy, Spain and other popular destinations will go a long towards supporting the Greek economy.

If the Greek people can convince themselves that this would be a plausible alternative, then they could make a few demands on the troika. First, they could say that ten years of continuous austerity is not acceptable.

Yes, the Greeks had been reckless borrowers, but the European banks had also been reckless lenders. It is true that the Greek government had lied about its budget situation. But the word among finance types is that everyone knew they were lying and went along with the joke. Goldman Sachs even designed a nifty swap that allowed it to profit from the lies.

Instead of austerity, the Greek people might insist that the ECB focus on a growth agenda. This would mean that the ECB would have to ditch its obsession with a 2% inflation target and start acting like a real central bank. The ECB could start by guaranteeing the debt of Italy and Spain, both of which risk a rising interest rate/debt default death spiral, if there is not a credible guarantee behind their debt.

It might also start pushing more expansionary policies. It's always hard to admit when you are wrong, but the ECB-IMF policy of growth through austerity is not working. Every month, we get more proof of this fact - with data showing that growth is lower than expected and unemployment is higher than expected. Is there any evidence that could get these people to change their minds before they destroy Europe's economies? Maybe, the Greek people could have forced the troika to actually look at the data.

There would have been other potential for fun in these negotiations. The Greek people, who have already been forced to accept a rise in their retirement age and lower pensions, may suggest the same for IMF economists. These hard-working types can often retire from their jobs in their early 50s. Instead of the meager Greek pensions of a few hundred euros a month that got the banker types so riled, the IMF crew can be pocketing close to $10,000 a month in their pensions. Perhaps IMF pensions would have come up for debate, if the Greek people actually had to be convinced that a bailout was in their own good.

But the chance to bring the Greek people into the discussion was quickly nixed. We are back to a conversation among the bankers and the politicians. There is not much room for democracy in this story, but we can still dream.

Greek Prime Minister George Papandreou touched off a firestorm last week when he proposed putting the austerity package designed by the "troika" (the IMF, the European Central Bank and the European Union) up for a popular vote. The idea that the Greek people might directly be able to decide their future terrified leaders across Europe and around the world. Financial markets panicked, sending stocks plummeting and bond yields soaring.

However, by the end of the week, things were back under control. The leaders of France and Germany apparently laid down the law to Papandreou and he backed off plans for the referendum. While the government is in the process of collapsing in Greece, the world can now rest assured that the Greek people will not have an opportunity to vote on their future.

This is unfortunate, since it means that Greece's future will likely be decided by politicians who may not have the interests of the Greek people foremost in their minds. By their own projections, the austerity package designed by the troika promises a decade of austerity, with high unemployment, falling real wages and sharp reductions in public services and pensions. And their projections have consistently proven to be overly optimistic.

If given the opportunity, would the Greek people endorse this sort of austerity package? The answer obviously depends on the alternative.

The alternative route almost certainly means a disorderly debt default and a departure from the euro. That is not a pretty picture. If Greece follows the path of Argentina, the last country to make a similar break, then the economy is likely to undergo a free fall for a period of time. The duration of this free fall will depend on how long it takes the government to get a new currency in use and construct some provisional formula for converting euro-denominated contracts into the new currency.

In Argentina, this period was three months, with another three months of stagnation before the economy began a sustained boom. The process could be more difficult in Greece, both because it is tied in more extensively to the eurozone countries, and because Argentina at least had its own currency.

However, even in the case of Greece, such a break would not be impossible. There would be a desire to hold the new currency. The government just has to impose a new property tax, which is only payable in the new currency.

People will want to hold onto ocean-front property in the Greek islands or at the foot of the Acropolis, so there will be demand for the currency. Also, the prospect of a tourist boom, once prices in Greece fall by 50% relative to Italy, Spain and other popular destinations will go a long towards supporting the Greek economy.

If the Greek people can convince themselves that this would be a plausible alternative, then they could make a few demands on the troika. First, they could say that ten years of continuous austerity is not acceptable.

Yes, the Greeks had been reckless borrowers, but the European banks had also been reckless lenders. It is true that the Greek government had lied about its budget situation. But the word among finance types is that everyone knew they were lying and went along with the joke. Goldman Sachs even designed a nifty swap that allowed it to profit from the lies.

Instead of austerity, the Greek people might insist that the ECB focus on a growth agenda. This would mean that the ECB would have to ditch its obsession with a 2% inflation target and start acting like a real central bank. The ECB could start by guaranteeing the debt of Italy and Spain, both of which risk a rising interest rate/debt default death spiral, if there is not a credible guarantee behind their debt.

It might also start pushing more expansionary policies. It's always hard to admit when you are wrong, but the ECB-IMF policy of growth through austerity is not working. Every month, we get more proof of this fact - with data showing that growth is lower than expected and unemployment is higher than expected. Is there any evidence that could get these people to change their minds before they destroy Europe's economies? Maybe, the Greek people could have forced the troika to actually look at the data.

There would have been other potential for fun in these negotiations. The Greek people, who have already been forced to accept a rise in their retirement age and lower pensions, may suggest the same for IMF economists. These hard-working types can often retire from their jobs in their early 50s. Instead of the meager Greek pensions of a few hundred euros a month that got the banker types so riled, the IMF crew can be pocketing close to $10,000 a month in their pensions. Perhaps IMF pensions would have come up for debate, if the Greek people actually had to be convinced that a bailout was in their own good.

But the chance to bring the Greek people into the discussion was quickly nixed. We are back to a conversation among the bankers and the politicians. There is not much room for democracy in this story, but we can still dream.